The economy had already been weakening, with minimal job growth in 2025 and a deceleration in GDP. Inflation had been decelerating but remained above the Federal Reserve’s target. In this research note, we examine fixed income sector performance in the first quarter. We also note what a continuation of mildly elevated inflation, combined with slowing growth, could mean for fixed income investing over the next quarter and the remainder of the year. We do so in the context of explicit inflation protection, broader investment considerations suited to this environment, and the corporate sectors best positioned to outperform.

First Quarter Fixed Income Performance

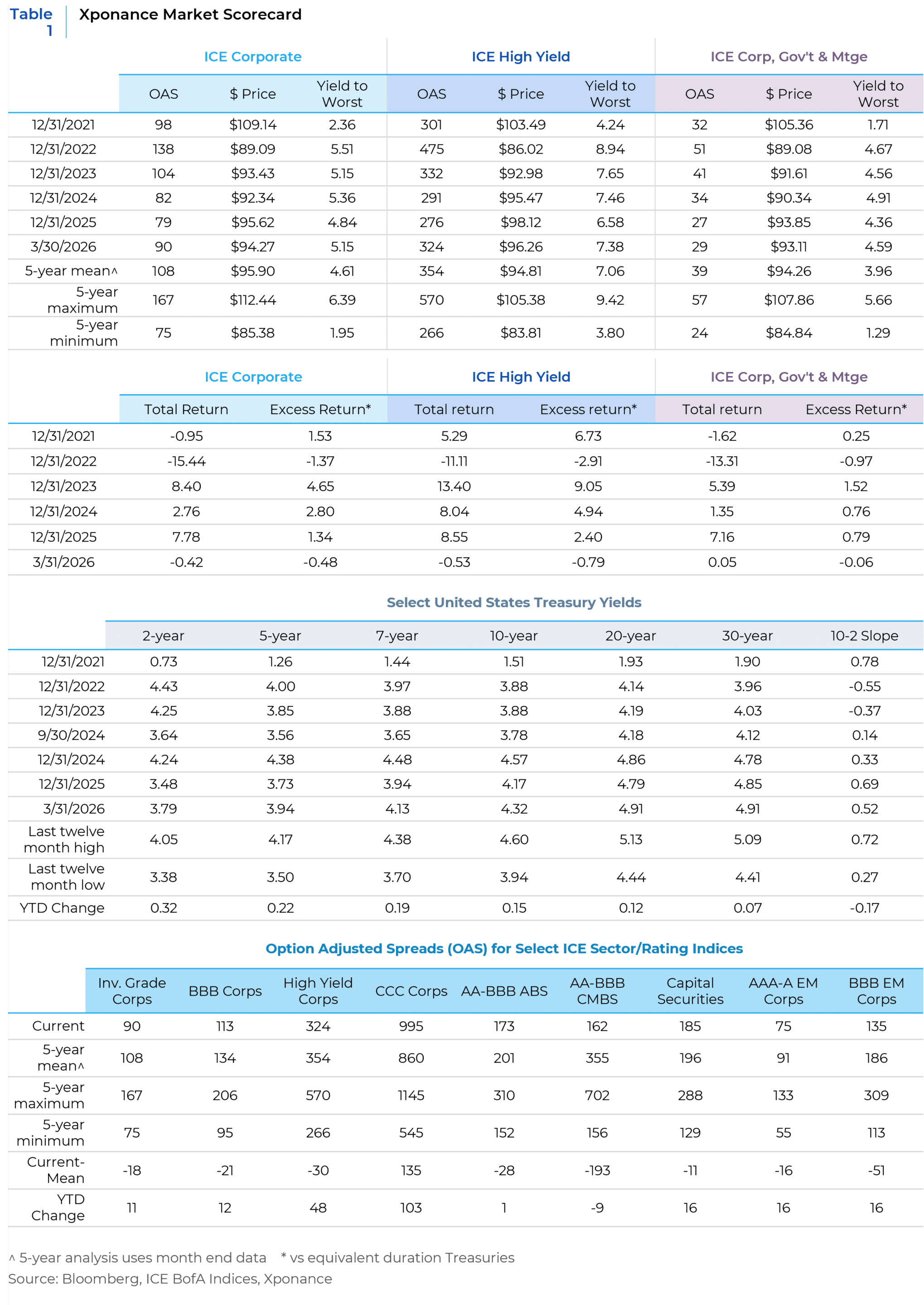

In the first quarter of 2026, market performance was more volatile than at any point since the “Liberation Day” in the second quarter of 2025. Across fixed income sectors, securitized assets were clear outperformers. While the Bloomberg Aggregate Index was slightly negative on a total return basis for the quarter (-5 bps), agency MBS generated 40 bps of total return, and both ABS and CMBS returned just over 30 bps.

Corporate bonds posted a negative total return of 54 bps, with dispersion across sectors significantly higher than in recent quarters. The trading environment was not characterized by indiscriminate risk-off selling, but rather by a differentiated sell-off reflecting both the impact of the war in Iran and evolving U.S. economic fundamentals. Despite rising rates, coupon income helped limit downside for U.S. Treasuries, leaving total returns only modestly negative and slightly outperforming the broad index by 1 bp.

Corporate Sector Differentiation

Corporate sub-sector performance was one of the most notable developments of the quarter, as differentiation both across and within sectors returned in force. As expected, Energy was the top-performing broad sector in the index, posting 12 bps of total return. Within Energy, Independent producers (i.e., companies primarily focused on oil and gas production) led performance, generating 63 bps of total return. Along with Oilfield Services and Refining, this group was among the few sub-sectors to post positive returns for the quarter.

On the negative side, Media/Entertainment and Leisure were the worst-performing sectors, each declining by 90 bps or more. Weakness in Media/Entertainment was largely driven by sector-specific event risk, while Leisure was more directly impacted by the war. Consumer Cyclical Services, as well as select Consumer Staples segments (notably Food & Beverage and Supermarkets), also underperformed the broader index. We attribute this, in part, to the secondary effects of the conflict, as higher gasoline prices have begun to alter consumer behavior.

Stagflation Risks and Global Supply Dynamics

Given the economic headwinds facing the U.S. even prior to the outbreak of the war in Iran, we remain concerned about the potential for mild stagflation. The Iran war could foster another classic supply-driven inflationary episode—driven not only by oil prices, but also by a range of second-order effects stemming from both oil and global LNG markets (as distinct from U.S. LNG).

These inputs feed into a wide array of products, including, most notably, fertilizers and plastics. Moreover, current conditions could begin to echo the dynamics seen during the COVID period, when supply chain bottlenecks led to widespread shortages and a corresponding increase in prices. Taiwan, for example, is the primary global supplier of advanced semiconductors while also relying heavily on imported energy—much of it in the form of LNG—underscoring the potential for energy disruptions to cascade through critical global supply chains.

Global Growth and IMF Perspective

The United States has been relatively insulated from the effects of the war compared to the rest of the world—a point recently highlighted by the International Monetary Fund (IMF) in its latest downgrade of global growth forecasts. In its April 2026 World Economic Outlook, the IMF revised its global growth projection to 3.1%, down from 3.4% in its October 2025 report. This downgrade largely reflects heightened inflationary pressures in Europe, Asia, and other energy-importing regions.

The IMF also outlined downside scenarios, including an adverse case in which global growth slows to 2.5% and a severe scenario in which growth declines to 2.1%. These scenarios correspond to average Brent crude prices of approximately $100 and $110 per barrel, respectively, for 2026. For context, global growth of 2.0% is typically associated with recessionary conditions, while the 50-year average growth rate is approximately 3.0%.

We highlight these figures to emphasize that much of the financial press tends to interpret global developments through a U.S.-centric lens. As a result, the broader impact of the war on global supply chains and the international economy has, in our view, been somewhat underappreciated.

Inflation Protection and TIPS Analysis

Even prior to the outbreak of war, discussions around stagflation had become increasingly prevalent in our conversations with allocators, consultants, and other market participants. A natural extension of these discussions has been the role of explicit inflation protection, particularly through Treasury Inflation-Protected Securities (TIPS). While TIPS are not included in major bond indices, they exhibit core-like characteristics in terms of credit quality, duration, and portfolio utility.

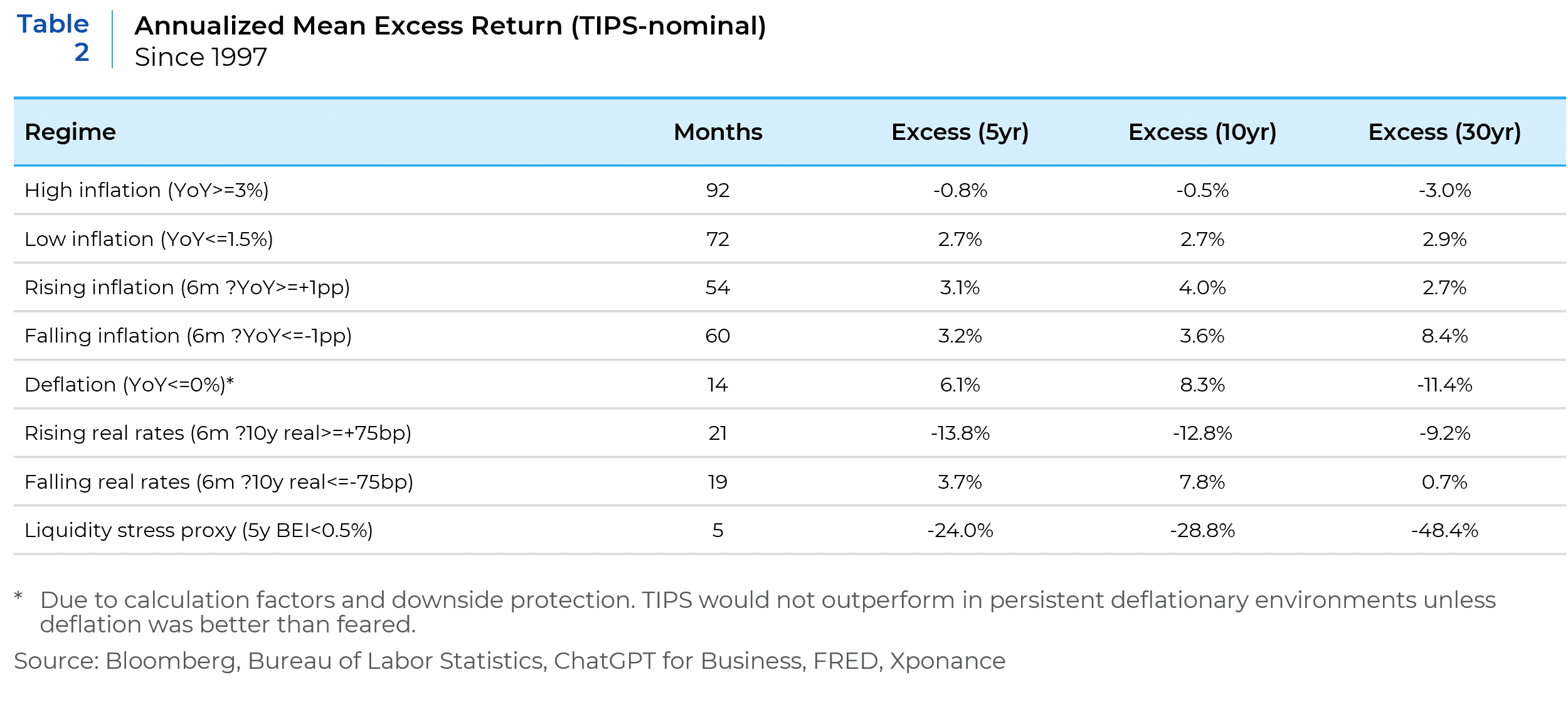

Against a backdrop of persistently above-target inflation (i.e., in the 2–4% range), we conducted a refreshed analysis of TIPS relative to nominal U.S. Treasuries since inception, with particular focus on the post-COVID period. An important distinction in this comparison is the difference between TIPS price performance and the mechanics of inflation compensation. Breakeven inflation rates represent the level at which nominal Treasuries and TIPS would generate equivalent returns; however, both empirical research and intuition suggest that liquidity premia and inflation risk premia (analogous to nominal term premia) play a meaningful role in driving TIPS performance.

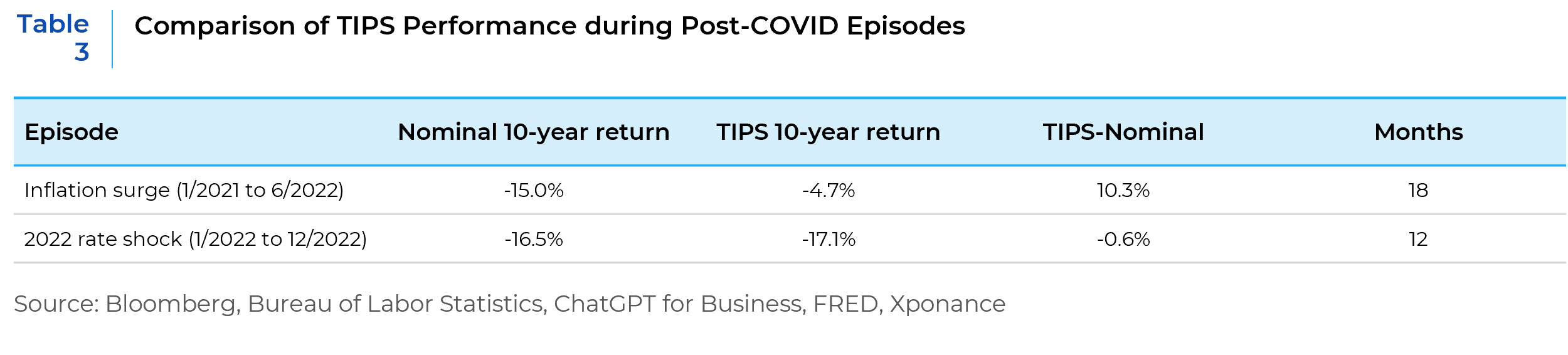

Focusing on the post-COVID period, these dynamics become clear. The initial phase of elevated inflation produced a markedly different return profile for TIPS compared to the subsequent period, during which both nominal and real interest rates rose significantly as the Fed raised rates in an effort to “break the back” of inflation. This latter phase bears resemblance to the policy response seen during the Volcker era of the late 1970s and early 1980s.

Extrapolating from the TIPS regime analysis above, there is a compelling case for the outperformance of intermediate-term Treasury Inflation-Protected Securities as part of a fixed income toolkit in the current environment. The regime framework suggests that prevailing U.S. economic conditions—characterized by mildly elevated inflation without a pronounced monetary tightening bias—support the role of TIPS as both a diversifier and a potential return enhancer relative to nominal Treasuries, based on historical experience.

A key takeaway from this analysis, however, is that TIPS tend to underperform in environments where real rates rise sharply. In other words, if inflation reaches levels that prompt aggressive monetary tightening, or if inflation expectations drive a significant increase in real yields, the duration-driven price declines can overwhelm both the inflation adjustment and the typically lower coupon profile of TIPS.

Beyond a dedicated allocation to TIPS, more traditional fixed income instruments will also play an important role in portfolios under these conditions, as discussed below.

Interest Rate Outlook and Curve Positioning

We continue to expect the Treasury curve to steepen in response to the apparent slowdown in economic growth. Interest rate options are currently pricing in less than a full rate cut in the federal funds rate by year-end 2026. As a result, movements along the curve may resemble a modest bull steepener, with front-end yields declining slightly while the 10-year remains range-bound near current levels.

At the long end, the 30-year yield has the potential to move higher, reflecting the impact of elevated deficit spending following last year’s OBBBA tax cut extension, as well as increased funding needs to replenish military stockpiles depleted during the war in Iran. More broadly, term premia have re-emerged across developed markets alongside the return of inflation and the end of the zero interest rate policy era. There is little reason to expect this trend to reverse.

Securitized Sector Positioning

From a broad sector perspective, and within this potentially muted rate backdrop, increasing exposure to agency mortgage-backed securities (MBS) appears attractive. This view is supported not only by their historically strong risk-adjusted performance in downside scenarios, but also by the opportunity to generate alpha through careful analysis of prepayment dynamics—such as geography, servicer behavior, and pool-specific characteristics—particularly given the wide dispersion of coupons currently available in the market. Moreover, the “higher for longer” rate backdrop has led to muted MBS issuance, which presents an advantageous supply/demand imbalance in the current environment.

Within asset-backed securities (ABS), we have continued to avoid consumer-facing collateral, which dominates the sector. As noted in our first-quarter commentary, growth in esoteric ABS issuance has increasingly been tied to the data center buildout. We view this as better suited to equity investors, whose opportunity for outsized returns associated with the artificial intelligence investment cycle are better positioned to absorb potential downside risk in exchange. Given the asymmetric return profile of bonds, we believe such exposures are unsuitable for core fixed income portfolios.

Commercial mortgage-backed securities (CMBS) spreads have rebounded meaningfully from the lows observed in late 2023 and early 2024. While the sector is not entirely unattractive, we believe investors have been well served by trimming exposure into recent strength. Our relative value and fundamental analysis suggest that more attractive entry points are likely to emerge, particularly in private-label commercial real estate. According to data from S&P Global, delinquency rates and modifications continued to increase in 1Q26, reiterating that patience is key for conduit CMBS. That said, agency multifamily CMBS continues to offer relative value, though security selection and issuer/program considerations remain critical.

Corporate Credit Positioning

Although corporate credit spreads have largely retraced the widening that followed the onset of the war in Iran, differentiation across credits has increased meaningfully compared to the second quarter of 2025. However, we believe—consistent with current portfolio positioning—that higher beta sectors are not particularly attractive at this stage.

As a reminder, we evaluate sector-level spread ranges across each subsector of the corporate index, enabling us to assess relative upside and downside when constructing portfolios. Viewed through this framework, most sectors continue to appear unattractive, leading us to maintain a defensive posture in corporate credit given the current macroeconomic and geopolitical backdrop. This positioning emphasizes sectors such as utilities, aerospace and defense, and other non-cyclical industries, including waste management.

We also find recent primary market issuance to be more attractive than existing secondary bonds, as newly issued, on-the-run securities tend to offer greater liquidity. This flexibility is particularly valuable as it allows us to reposition more efficiently and add higher beta exposure opportunistically should spreads widen further.

Conclusion

We remain concerned about macroeconomic and geopolitical backdrop. Domestically these include vulnerabilities in private credit, stress within the lower tier of the “K-shaped” economy, lackluster job growth, the resumption of student loan payments and the uncertain long-term impacts of artificial intelligence. And we have already extensively discussed global macro risks from the Iran war.

Despite these challenges, U.S. yields remain attractive, and the domestic economy appears better positioned than many global counterparts to withstand the disruptions stemming from the war in Iran. Our portfolios are therefore positioned defensively while maintaining a yield advantage relative to their respective benchmarks.

This report is neither an offer to sell nor a solicitation to invest in any product offered by Xponance® and should not be considered as investment advice. This report was prepared for clients and prospective clients of Xponance® and is intended to be used solely by such clients and prospective clients for educational and illustrative purposes. The information contained herein is proprietary to Xponance® and may not be duplicated or used for any purpose other than the educational purpose for which it has been provided. Any unauthorized use, duplication or disclosure of this report is strictly prohibited.

This report is based on information believed to be correct but is subject to revision. Although the information provided herein has been obtained from sources which Xponance® believes to be reliable, Xponance® does not guarantee its accuracy, and such information may be incomplete or condensed. Additional information is available from Xponance® upon request. All performance and other projections are historical and do not guarantee future performance. No assurance can be given that any particular investment objective or strategy will be achieved at a given time and actual investment results may vary over any given time.