Summary

The shipping shutdown in the Strait of Hormuz is the second major geopolitical disruption to hydrocarbon markets in the past four years (following Russia’s invasion of Ukraine). Like the oil shocks of the 1970s, the reassessment of supply risk and price volatility that follows will catalyze long-term structural change. The shocks of 1973–74 and 1979 did more than drive inflation—they permanently altered how economies consume energy, how governments manage risk, and how capital is allocated. Power systems shifted from oil toward coal, nuclear and natural gas, and policymakers institutionalized energy security through strategic reserves and supply diversification. At the same time, the shocks exposed the fragility of the prevailing macro framework, contributing to the breakdown of postwar inflation stability and the eventual rise of modern central banking focused on inflation control.

The investment consequences were equally durable. Energy ceased to be a stable input and instead became a strategic variable embedded in asset pricing and industrial policy. Capital flowed into new supply basins, eroding OPEC’s dominance, while financial markets evolved to hedge and price energy risk more explicitly. Public policy and private sector investments responded by reducing energy intensity and reconfiguring production, accelerating a broader shift toward less energy-dependent growth. Global energy usage per dollar of GDP, for example, declined by almost 40% since the 1980 oil price shock. In the U.S., oil per unit of GDP declined ~70% since 1980 and the U.S. eventually emerged as the world’s largest producer of oil and gas and a net energy exporter since 2019. Consequently, disruptions to oil and gas supplies now largely redistribute income within the U.S. economy, rather than drain its current account. That is not immunity — but it is a different, typically milder transmission mechanism than in the 1970s.

For global oil importers, especially emerging markets, the oil shocks of the 1970s created a lasting environment of FX volatility and economic vulnerability that continues to be reflected in spreads and risk premia to this day. Coming on the heels of the end of the gold standard, the petrodollar investment process which emerged led to the financialization of debt markets for emerging economies and set in motion a boom-and-bust debt cycle over the ensuing decades.

Similarly, the disruptions of the 2020s are unlikely to fade back into the pre-2020 equilibrium. These oil shocks are hitting the global economy amid historic technological change that has massively increased prospective demand for power generation, while fundamentally shifting the economy to favor renewables (despite the apparent animosity towards renewable energy sources from the Trump administration). Today’s backdrop also includes a post-pandemic reprioritization of supply chain resilience over globalized efficiency as well as an explosive growth in government debt amid the advanced economies over the past two decades.

We believe the energy supply shocks of the 2020s will ultimately prove no less revolutionary for financial markets than their 50-year-old cousins did. Much like the First and Second World Wars culminated in the localization of steel production, over the next two decades, we believe that the shocks of the 2020s will accelerate the use of alternative energy sources for economically critical energy needs, culminating in the eventual end of dependence on globally traded hydrocarbons for economically critical energy needs. In countries with relative political and market stability, this shift could lower risk premia and create a virtuous circle for economic growth.

Much like the First and Second World Wars culminated in the localization of steel production, over the next two decades, we believe that the shocks of the 2020s will accelerate the use of alternative energy sources for economically critical energy needs.

Even before the price spikes of the Iran war, unsubsidized new utility-scale renewable energy projects had become more cost efficient than new fossil fuel-based power generation in most global jurisdictions. Even where they are not, it is most often due to policy or grid constraints that can (and likely will) be rectified, not imbalances in project economics. Fossil fuel projects dependent on local supply, such as coal plants in China, India, and Indonesia, or oil/gas in oil exporters will persist in the medium-term, but we believe that the supply shocks of the 2020s will sap nearly all remaining support for expanding grid dependence on imported hydrocarbons. We think this upside remains underappreciated by financial markets. Longer term, we believe that much like the oil shocks of the 1970s brought forward technologies in combined cycle gas turbines, fuel injection, heat pumps, and the computerization of vehicles, the oil shocks of the 2020s will bring forward new energy technologies as well. The most imminent revolution is likely to be in EV trucking, where global EV penetration rates still sit at only about 2% of the potential market, leaving the segment with the potential for $2-$3tn of global capex expenditures in the coming decade.1 Grid-scale battery storage, enhanced geothermal, hydrogen, and green ammonia are among the next frontier technologies to watch amid the coming revolution.

Where Will the Grid Lose Gas?

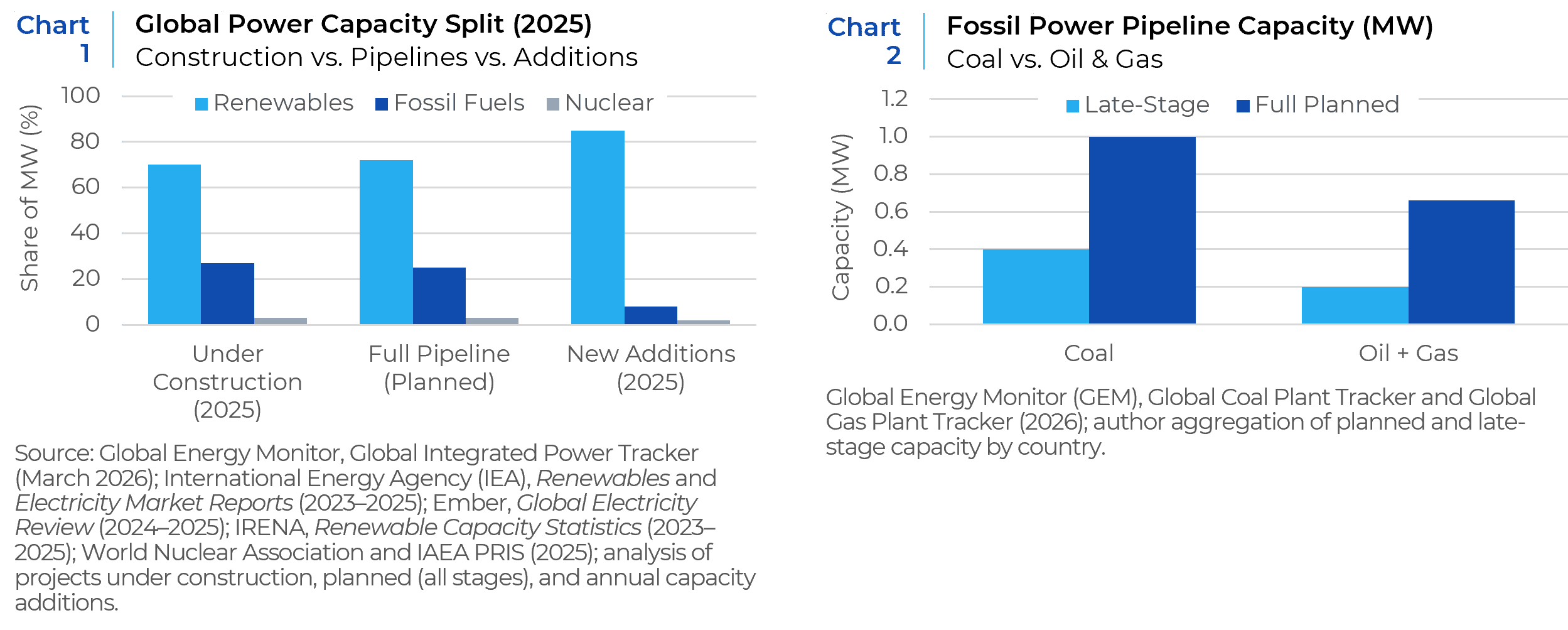

In 2022, on the back of the massive spike in oil prices (Brent Crude surged from $70/bbl to a peak of $127/bbl in 2022, exactly as it did in 2026), the share of global renewable energy projects under construction surged from less than half of the total (by total GW) to nearly 70% today. And as many renewable energy projects have shorter construction times than utility-scale fossil fuels, the total amount of added grid power in 2025 was dominated by renewables, at nearly 90% (see Chart 1)!

While renewable energy projects already dominate the global pipeline of power plant construction, fossil fuel plants still represent an estimated $2 trillion of potential capital investment that could be canceled or diverted in an environment of higher oil prices. But not all of these are equally at risk. In fact, coal plants comprise well over 60% of all fossil fuel plants being planned (see Chart 2), led of course by China and India (themselves already large producers and users of coal). Not only should investors not expect the current oil price disruptions to curtail these plans, but they may also be accelerated or expanded if a long-term repricing of oil/gas supply chain risk forces policymakers and planners to reset their priorities.

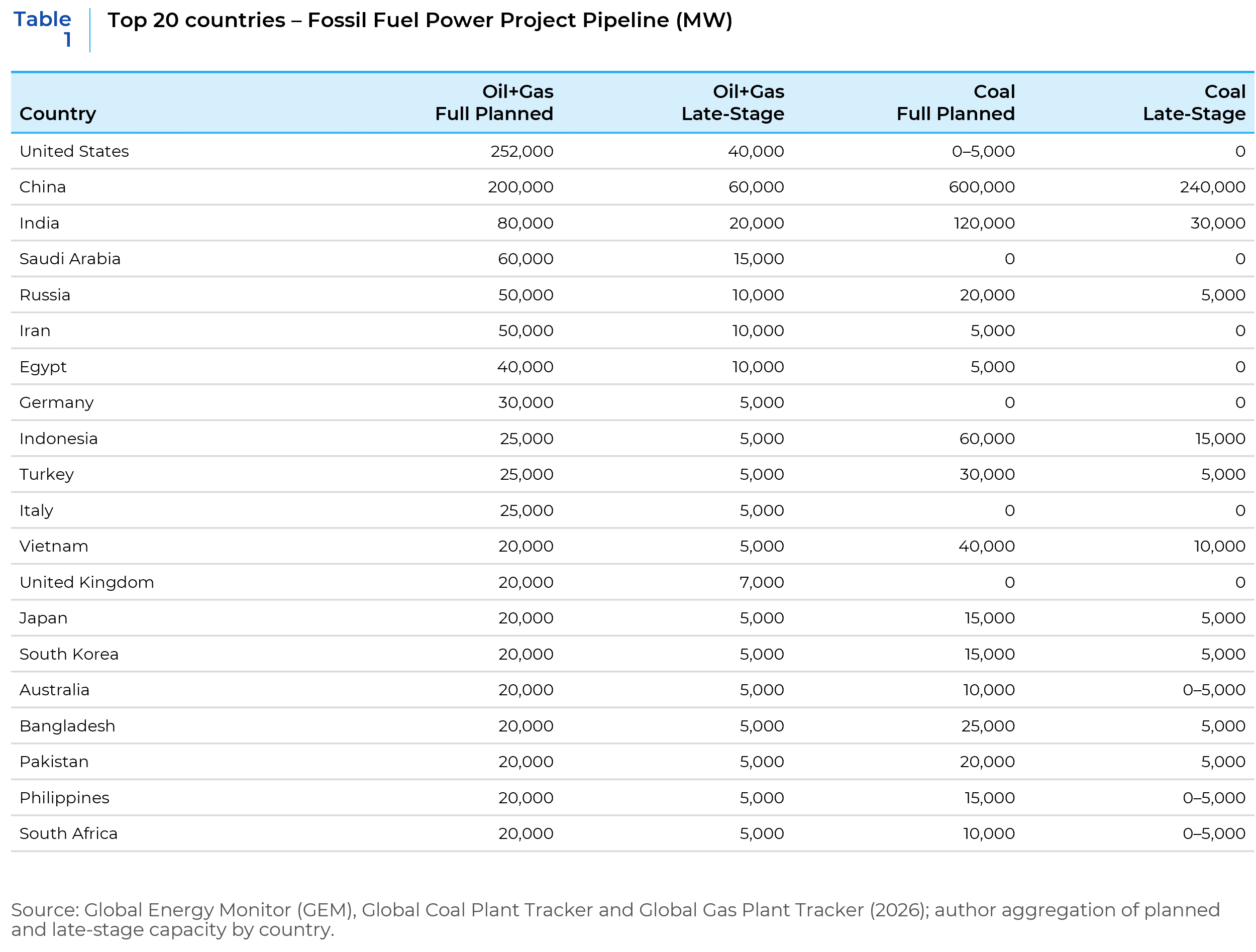

Breaking down the list of planned projects further, reveals that the vast majority of estimated future construction of gas-fired plants are in China – where state planning priorities can easily trump standard project economics – and oil/gas producing countries (see Table 1) led by the U.S. These projects should also prove stickier to abandon even in the face of higher for longer oil and gas prices and are clearly not subject to the same risks of global supply disruption.

Where we would expect to see the biggest potential changes in plans to future utility-scale power construction is from the oil importers on this list– Bangladesh, Egypt, Pakistan, the Philippines and Turkey in emerging markets, as well as Germany, Japan, Korea, and the UK in developed markets. Among the emerging economies, solar is already largely commercially viable in Egypt and Turkey, though development remains slow due to frictions in permitting and offtake guarantees. Pakistan, the Philippines, and Vietnam, are markets where shifting policy priorities brought by the current supply disruptions would have the most potential to unlock meaningful changes in future project economics.2 For the developed markets, deployment of utility-scale renewable energy has long already been a priority, and it is here where analysts should expect the most obvious upside for unpriced growth in renewable build-outs. In Japan, the changing political winds appear all but certain to lead to a substantial re-emergence of nuclear power in the coming years.

Reversing A 50-Year Legacy

Each year renewable power plant construction far outstrips fossil fuel plant construction, the global grid will gradually reduce the long-term marginal cost for power. Though this could be deflationary for consumers and industrial users, we believe that power demand will continue to grow alongside supply (or even far ahead of it, as we see today) for decades to come, as it essentially has for the past 200 years. But the changing mix of power sources will bring meaningful price stability in power generation, especially in emerging markets where historically these prices are the most unstable. This in turn is likely to reduce economic volatility, lower risk premia, extend investment horizons, and create a virtuous circle for development, where the political economy creates the necessary pre-conditions. The oil shocks of the 1970s created an environment of escalating risk for oil importers, especially in emerging markets. The long-term outcome of the oil shocks of the 2020s may bring the opposite.

- The subject of a future paper by Xponance.

- Bangladesh’s own political turmoil and weak policy framework make multi-year forecasts subject to more local political risk than is our focus here.

This report is neither an offer to sell nor a solicitation to invest in any product offered by Xponance® and should not be considered as investment advice. This report was prepared for clients and prospective clients of Xponance® and is intended to be used solely by such clients and prospective clients for educational and illustrative purposes. The information contained herein is proprietary to Xponance® and may not be duplicated or used for any purpose other than the educational purpose for which it has been provided. Any unauthorized use, duplication or disclosure of this report is strictly prohibited.

This report is based on information believed to be correct but is subject to revision. Although the information provided herein has been obtained from sources which Xponance® believes to be reliable, Xponance® does not guarantee its accuracy, and such information may be incomplete or condensed. Additional information is available from Xponance® upon request. All performance and other projections are historical and do not guarantee future performance. No assurance can be given that any particular investment objective or strategy will be achieved at a given time and actual investment results may vary over any given time.