Institutional equity portfolios have long been organized around the style box framework, splitting allocations between dedicated growth and value managers. While useful for classification, this structure introduces hidden costs, including forced turnover at index reconstitutions, duplicative holdings across benchmarks, and the behavioral drag of rebalancing away from recent winners into lagging segments. These inefficiencies are becoming more pronounced in today’s market. AI driven opportunities increasingly span the full style spectrum; interest rates have compressed traditional growth premiums, and geopolitical uncertainty continues to blur the line between value and growth leadership. As a result, rigid style mandates risk leaving investors structurally underexposed to meaningful sources of return.

This paper makes the case that core equity allocations offer a more efficient framework. Drawing on regime analysis, holdings overlap studies, turnover data, and comparative portfolio scenarios, we show that incorporating a core component delivers comparable or superior risk-adjusted returns while reducing costs, simplifying oversight, and providing the flexibility to allocate across the full valuation spectrum within a single mandate.

Style Investing versus Core Investing

Style investing refers to portfolio strategies that focus on securities exhibiting characteristics associated with either value or growth. Value investing emphasizes companies that appear undervalued relative to fundamentals such as earnings, book value, or cash flows, while growth investing focuses on firms expected to generate above-average earnings or revenue growth and often trade at higher valuation multiples. These approaches are grounded in academic finance, particularly in factor models such as the Fama-French framework, which identifies value and size as key drivers of long-term equity returns.

Core investing seeks to construct portfolios that reflect the broader equity market by blending value and growth exposures within a single mandate. Rather than concentrating on a single style, core strategies emphasize companies with balanced characteristics across valuation and growth dimensions. Core portfolios often resemble broad market benchmarks, while still allowing active managers to exploit security-specific opportunities.

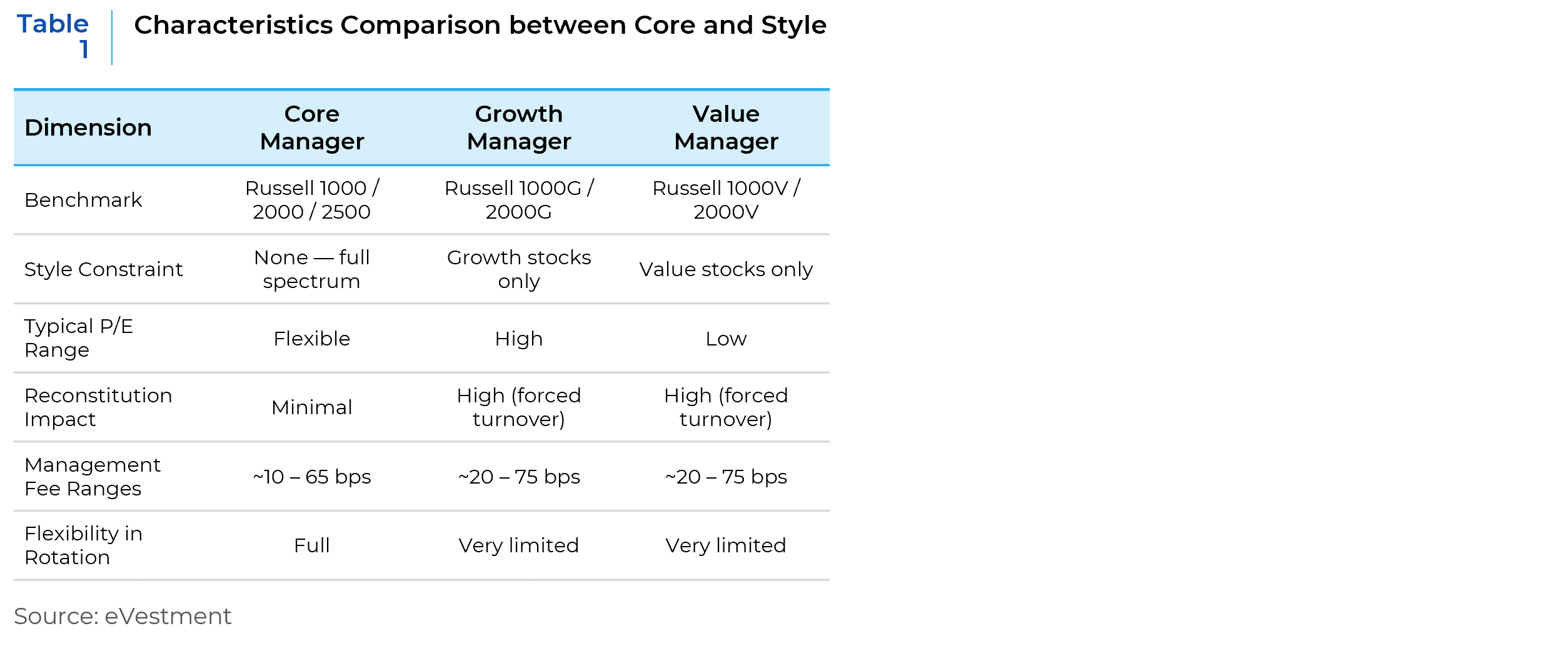

Table 1 highlights these practical differences. Core managers are typically benchmarked against broad indices such as the Russell 1000 or 2000 without a style constraint, allowing greater flexibility in portfolio rotation and access to the full range of valuation multiples. In contrast, growth and value managers operate within style-specific benchmarks and are more exposed to reconstitution effects, which can lead to higher levels of forced turnover. Core strategies also tend to have lower institutional fees than style-focused approaches.

Why Core Has the Edge Now

While style investing may capture factor premia over long horizons, it also introduces structural risks tied to shifts in market leadership. Performance leadership between value and growth rotates over time in response to macroeconomic conditions, interest-rate cycles, technological innovation, and changing investor expectations. Growth stocks, for example, dominated during the technology-driven expansion of the 2010s, while value has historically performed better in periods of economic recovery or rising inflation. As seen in Chart 1, periods of value outperformance are often followed by growth leadership, and vice versa, underscoring the cyclical nature of style returns.

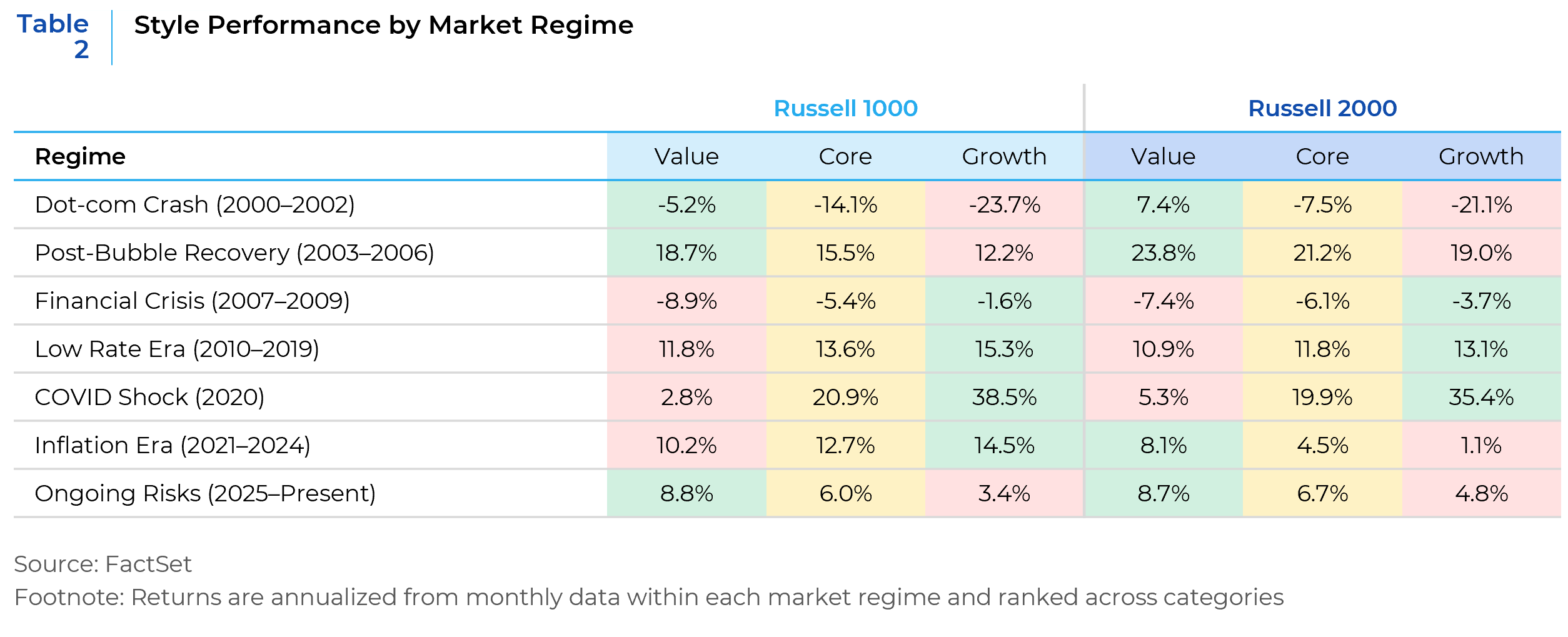

The regime-based analysis in Table 2 underscores the cyclical nature of style leadership across different macroeconomic environments. Periods of growth outperformance have typically coincided with low interest rates, innovation-driven environments, while value has tended to perform better during inflationary periods and the early stages of economic recovery. However, these shifts in leadership are difficult to anticipate in real time and can persist for extended periods before reversing. As a result, investors with concentrated exposure to a single style may experience prolonged periods of relative underperformance when leadership changes. By contrast, core strategies maintain continuous exposure across styles, reducing reliance on correctly anticipating shifts in market leadership. This balanced approach helps mitigate the impact of style cycles and supports more consistent performance across varying market environments.

The difficulty of timing style rotations is particularly relevant in today’s market environment. Inflation has moderated but remains uncertain, interest rate expectations continue to evolve, and the economic outlook is mixed. At the same time, elevated investment in artificial intelligence is supporting segments of the growth market, while geopolitical risks and policy uncertainty may favor more cyclical, value-oriented sectors such as energy and defense. These competing forces underscore how different parts of the market are being driven by distinct and, at times, opposing catalysts. A core approach provides a more reliable way to navigate this uncertainty by maintaining balanced exposure across styles. This allows investors to participate in evolving sources of return without relying on precise timing, reducing the risk of overconcentration in any one style and supporting more consistent outcomes across changing market conditions.

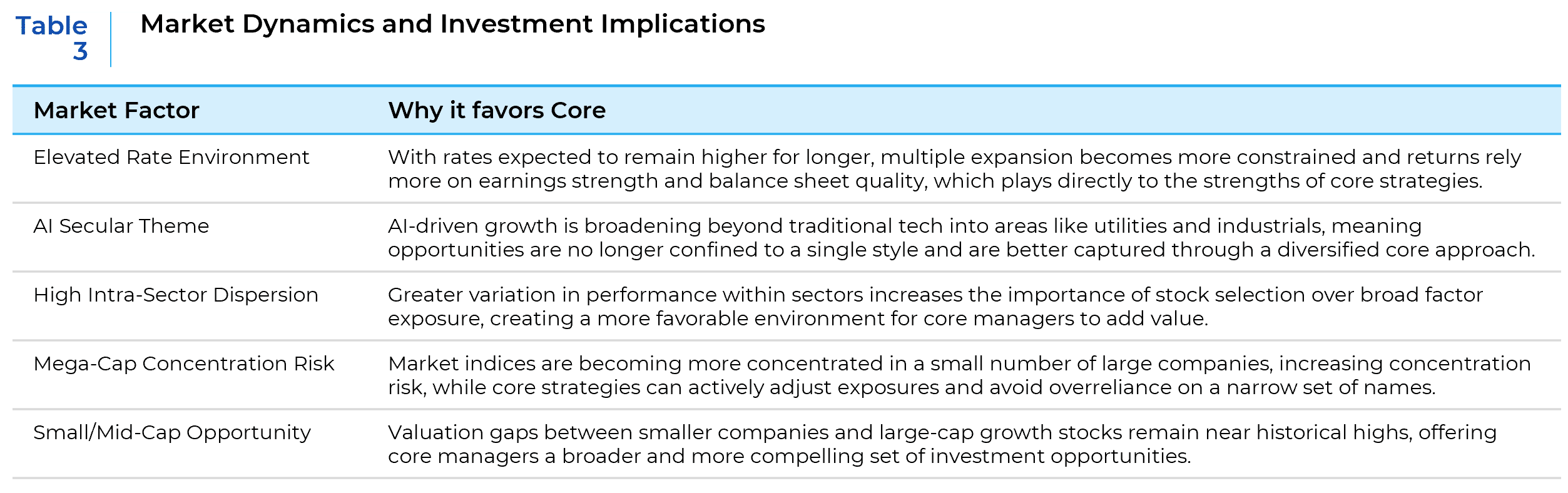

As of the first quarter of 2026, as highlighted in Table 3, several structural factors are aligning to favor core mandates over traditional style-based allocations. AI driven growth is increasingly broadening beyond traditional technology sectors into areas such as utilities and industrials, expanding the opportunity set across the market. At the same time, greater variation in performance within sectors is increasing the importance of stock selection over broad factor exposure. This is occurring alongside rising concentration in a small number of mega cap companies, as well as attractive opportunities emerging across small and mid-cap segments. In this environment, the managers best positioned to capture the full opportunity set are those able to allocate flexibly across styles, combining durable growth franchises with attractively valued cyclical businesses within a single portfolio.

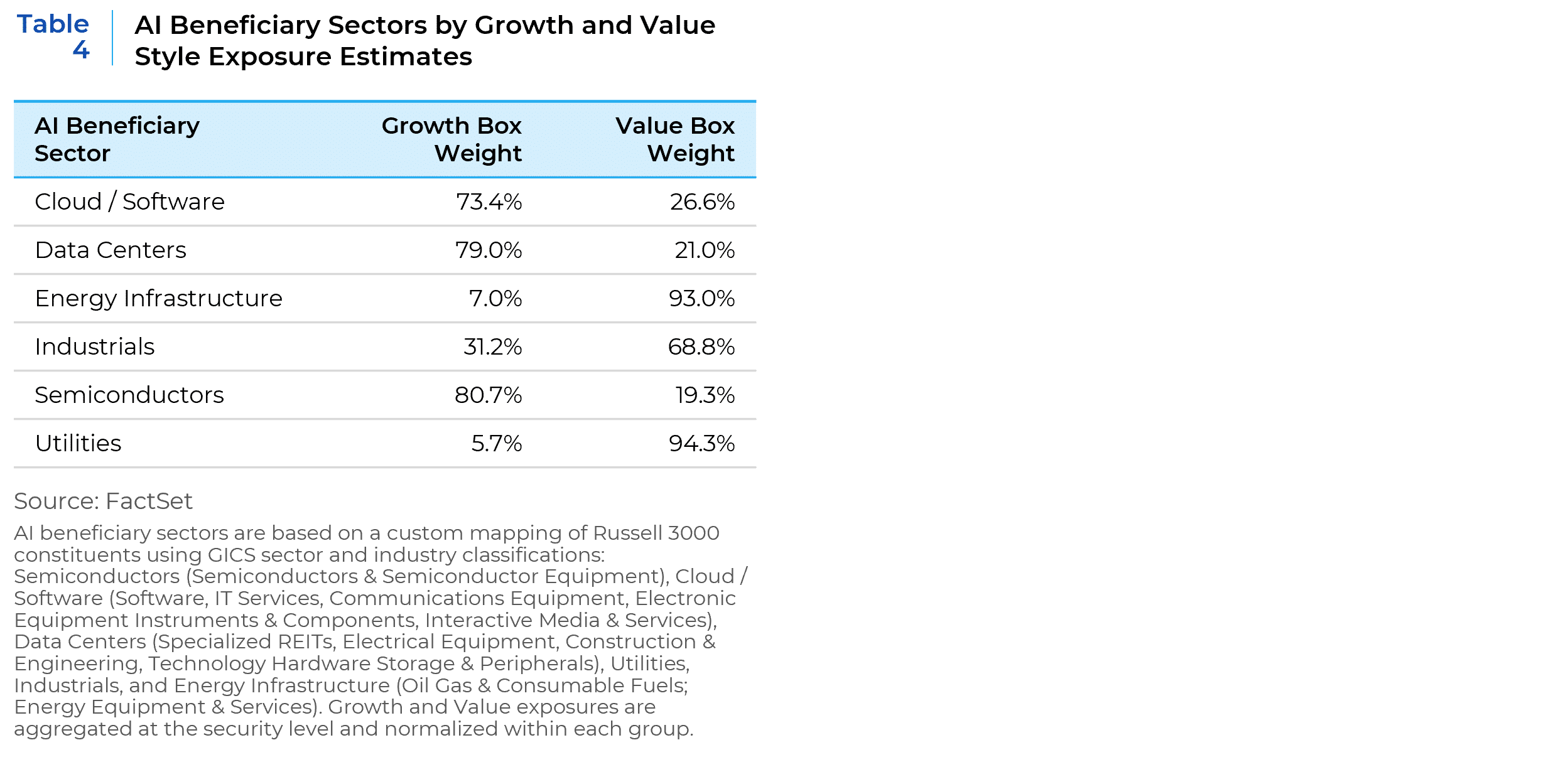

The AI-driven capital expenditure cycle serves as a particularly clear illustration of these dynamics in practice. Table 4 shows a sector-based decomposition of AI-related beneficiaries, where growth and value exposures are aggregated and normalized within each category to assess style composition. Segments such as Cloud and Software, Data Centers, and Semiconductors remain predominantly growth oriented, while Energy Infrastructure, Utilities, and Industrials exhibit a stronger value tilt. This dispersion across AI-linked segments highlights that leadership within the ecosystem is not confined to a single style and can shift as different parts of the value chain drive returns. As a result, style-constrained managers are inherently limited in their ability to capture the full opportunity set, whereas a core blend approach offers a structural advantage by providing consistent and comprehensive exposure to both growth and value beneficiaries of the AI cycle.

The Overlap Problem and Behavioral Considerations

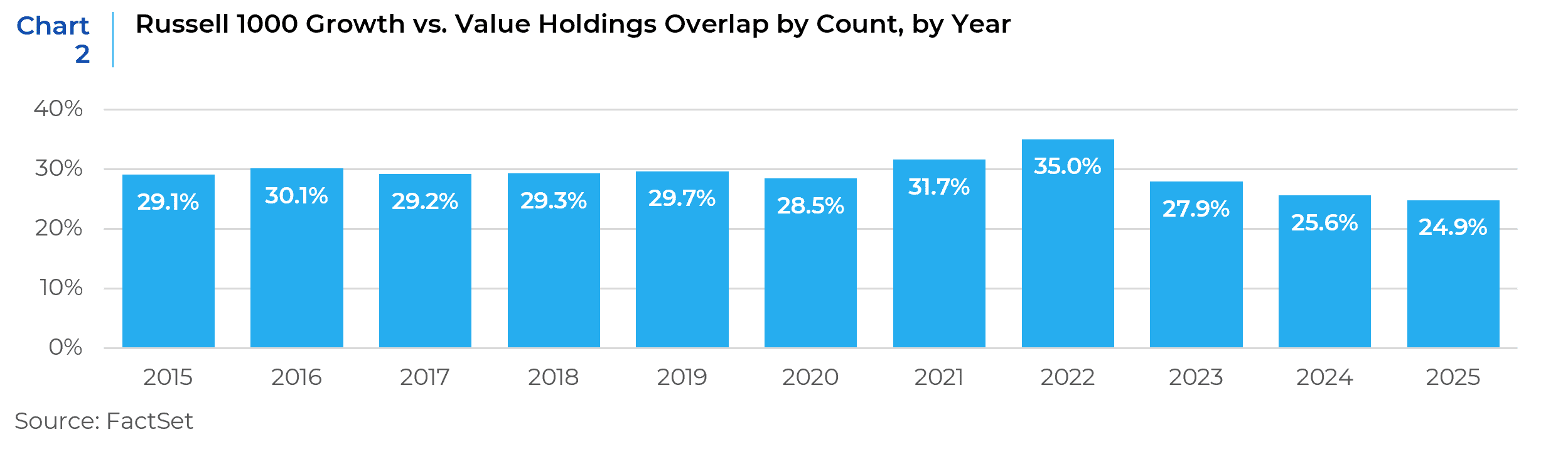

Importantly, style exposures are not as distinct as they are often assumed to be. While growth and value are typically treated as separate and complementary allocations, in practice there is a meaningful and persistent overlap in holdings between the Russell 1000 Growth and Russell 1000 Value indices. As illustrated in Chart 2 below, this overlap has consistently ranged between 25% and 35% over the past decade.

As a result, investors attempting to time or diversify across styles may end up with less differentiated exposures than intended. Even when employing separate managers to gain dedicated growth and value exposure, portfolios can still exhibit significant overlap at the security level. This reduces the effectiveness of style diversification and can lead to unintended concentration in common underlying drivers of risk and return, despite appearing well balanced across styles.

Style-split structures also introduce unintended behavioral challenges. When one style meaningfully outperforms the other, portfolio weights drift, with growth exposure rising while value declines. Rebalancing policies typically require trimming outperformers and reallocating them to lagging segments. While consistent with long-term discipline, these decisions are driven by relative performance rather than underlying fundamentals or manager conviction and may occur at inopportune times. By contrast, a core approach avoids these structural constraints. Without rigid style targets, a core manager can allocate capital within a unified framework. This reduces the likelihood of systematically selling recent winners to fund exposure to underperforming segments when market conditions do not support such shifts.

Reconstitution-Driven Turnover and Cost Implications

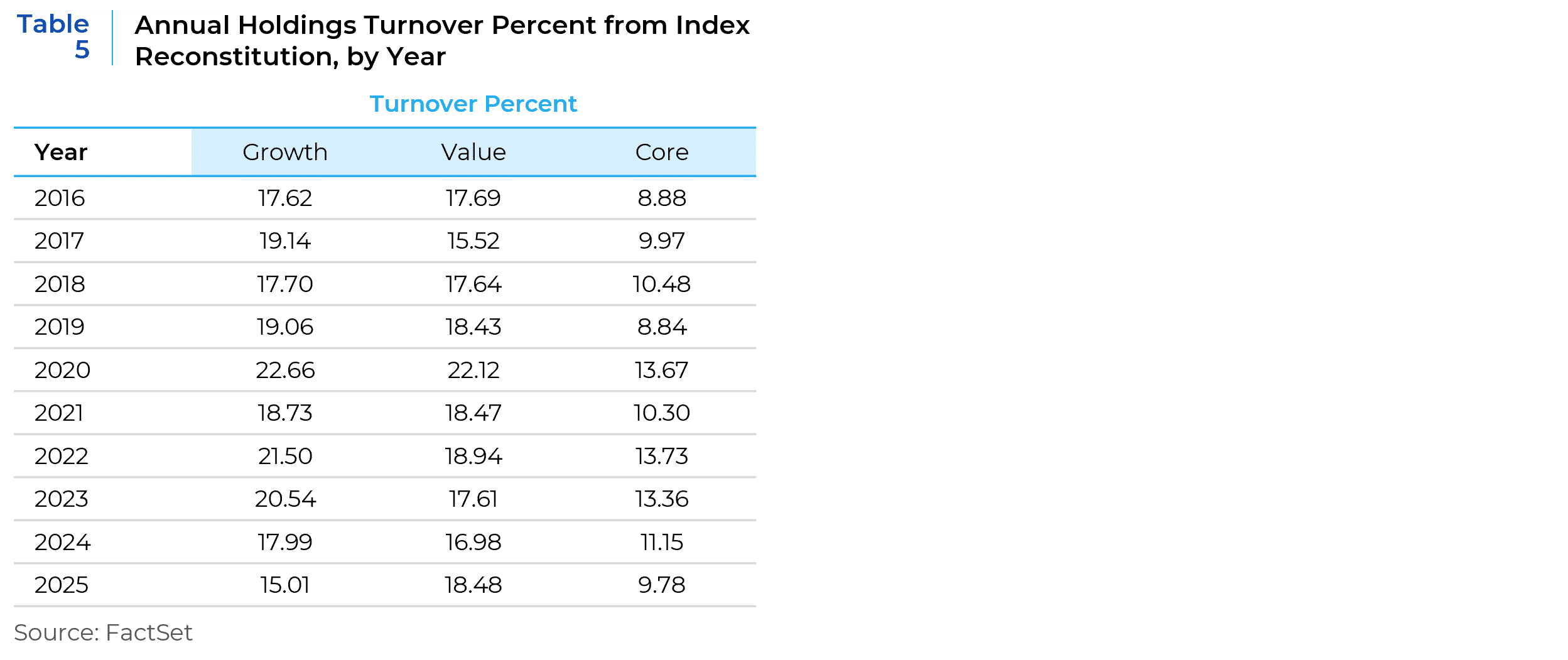

One of the most significant and often underappreciated costs of style investing arises from forced turnover during index reconstitution. The Russell indices rebalance annually each June, during which securities may shift between growth and value classifications or move across market capitalization segments. These changes typically trigger mechanical buying and selling within each style index, regardless of underlying fundamentals.

As shown in Table 5, turnover in both the growth and value indices has generally remained higher than in the core index. This difference has practical implications for portfolio construction, especially for managers that attempt to minimize tracking error relative to their style benchmark. Allocating across separate growth and value managers can lead to higher aggregate trading activity, as each strategy adjusts to classification changes. In contrast, a core manager, benchmarked to the full index, tends to experience less rebalancing-related turnover. Therefore, a core approach may offer a more efficient implementation, with lower turnover and potentially reduced transaction costs, while still providing broad market exposure

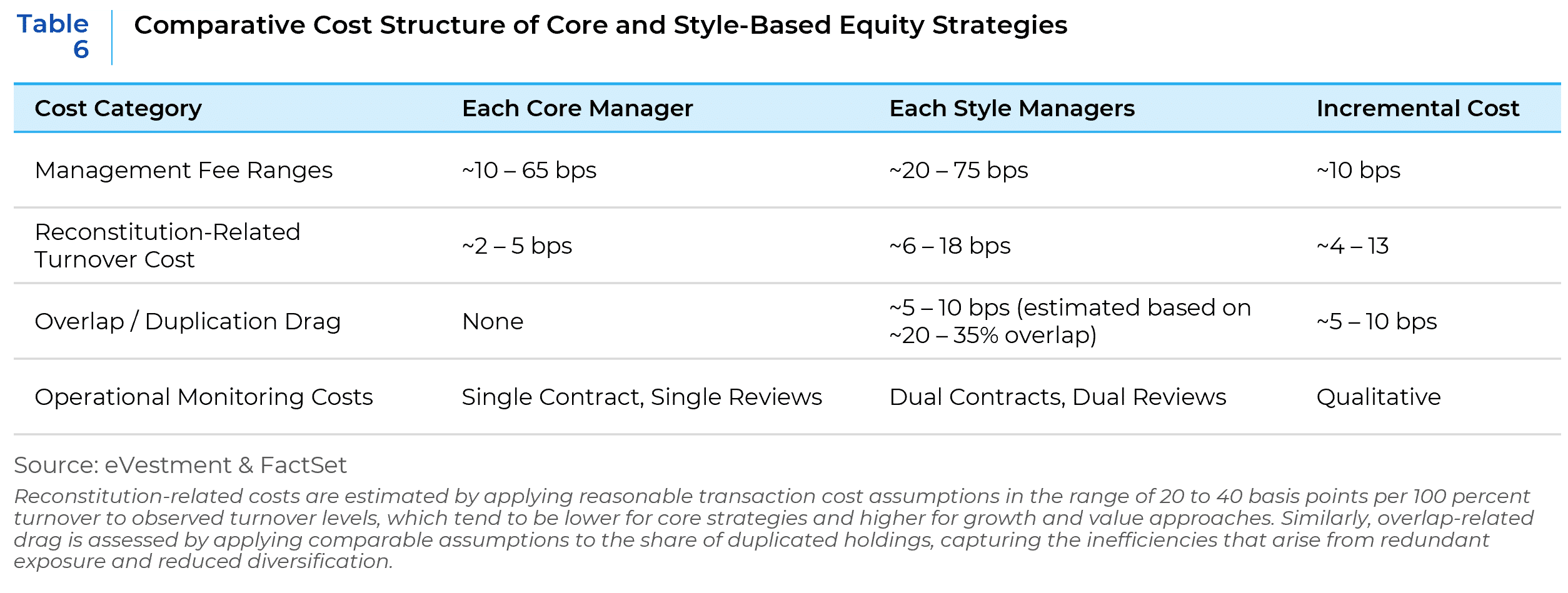

These differences in turnover represent only one dimension of the broader cost considerations associated with style-based allocations. While style-based allocations are often justified on diversification grounds, they can introduce multiple layers of cost that are not always immediately apparent. Table 6 provides a more detailed view of these cost components. Managing separate growth and value mandates also adds operational complexity, requiring additional oversight, coordination, and ongoing monitoring. Over time, these frictions can accumulate and weigh on performance, making style-based approaches less cost-efficient than they may initially appear. By contrast, adding a core strategy can deliver comparable market exposure through a more streamlined and efficient structure.

Evaluating the Effectiveness adding Core to Blended Style Portfolio

The following allocation examples, based on eVestment median manager data across the respective universes, illustrate how incorporating core strategies alongside growth and value exposures can improve overall portfolio outcomes. Across both a large-cap-only framework and a multi-cap allocation, the results show that portfolios incorporating a core component perform as well as or better than style-only approaches on both an absolute and risk-adjusted basis.

As summarized in Table 7, in the large-cap scenario, replacing a portion of the growth and value allocation with core results in comparable returns, while meaningfully reducing volatility and drawdowns. Sharpe ratios improve modestly, reflecting more efficient return generation per unit of risk. Extending the analysis to include mid-cap exposure reinforces this pattern. In the large-cap plus mid-cap framework, introducing core within each segment leads to slightly higher returns over longer horizons, accompanied by lower standard deviation and improved drawdown profiles. The incremental Sharpe ratio improvement suggests enhanced risk-adjusted performance, indicating that core allocations contribute to more efficient diversification across market capitalizations. A similar pattern emerges in the multi-cap framework, where introducing core across large, mid, and small-cap segments leads to small improvements in returns, lower standard deviation, and better downside protection. These results indicate that core allocations can enhance portfolio efficiency without sacrificing market exposure.

Importantly, these benefits extend beyond performance metrics. As discussed previously, style-based implementations are associated with higher turnover, greater overlap, and elevated transaction costs due to index reconstitution dynamics. By allocating a larger share of the portfolio to core strategies, investors can reduce reliance on separate growth and value mandates, thereby lowering aggregate trading activity and minimizing duplication across holdings. Given that core strategies generally exhibit lower turnover and lower fee structures than style-specific approaches, increasing core exposure can also contribute to reduced implementation costs over time.

Taken together, these findings suggest that incorporating core into a blended allocation not only improves risk adjusted outcomes but also enhances overall portfolio efficiency. Rather than relying solely on style segmentation, a core inclusive approach provides a more streamlined structure that captures broad market opportunities while mitigating both performance and cost related frictions. In today’s environment, elevated dispersion, broader opportunity sets, and persistent macro uncertainty are making the advantages of core not only structural but increasingly actionable. Allocators should consider increasing core exposure as a more resilient portfolio framework.

This report is neither an offer to sell nor a solicitation to invest in any product offered by Xponance® and should not be considered as investment advice. This report was prepared for clients and prospective clients of Xponance® and is intended to be used solely by such clients and prospective clients for educational and illustrative purposes. The information contained herein is proprietary to Xponance® and may not be duplicated or used for any purpose other than the educational purpose for which it has been provided. Any unauthorized use, duplication or disclosure of this report is strictly prohibited.

This report is based on information believed to be correct but is subject to revision. Although the information provided herein has been obtained from sources which Xponance® believes to be reliable, Xponance® does not guarantee its accuracy, and such information may be incomplete or condensed. Additional information is available from Xponance® upon request. All performance and other projections are historical and do not guarantee future performance. No assurance can be given that any particular investment objective or strategy will be achieved at a given time and actual investment results may vary over any given time.