Article Summary

Our 2Q Market Outlook “Reality “Trumps” the Reflation Trade,” evaluates the recent retreat in risk assets, trends in global equities, the impact of a strong U.S. dollar, and continued political uncertainty under the Trump Administration. Key points include:

- Policy expectations and synchronized global growth will continue to be the biggest market considerations for investors this year.

- The U.S. dollar will be critical in determining this year’s winners and losers.

Risk assets continued their relentless post-election march during the first two months of 2017. Buoyed by the selloff in the US dollar, emerging markets bested global markets in both US dollar and local currency terms. The Eurozone was a close second outperforming both the U.S. and the MSCI All-Country World Index (ACWI) in local currency terms. Japanese equities, however, halted their Q4 2016 gallop with a negative absolute return. On the sector front, tech came out on top consistently across regions while reports of elevated inventories as well as an unwinding of extreme net long positioning among both commercial and non-commercial traders led to negative energy sector performance. Health care, consumer discretionary and consumer staples outperformed the broad market, while financials, materials and telecom services trailed the MSCI ACWI.

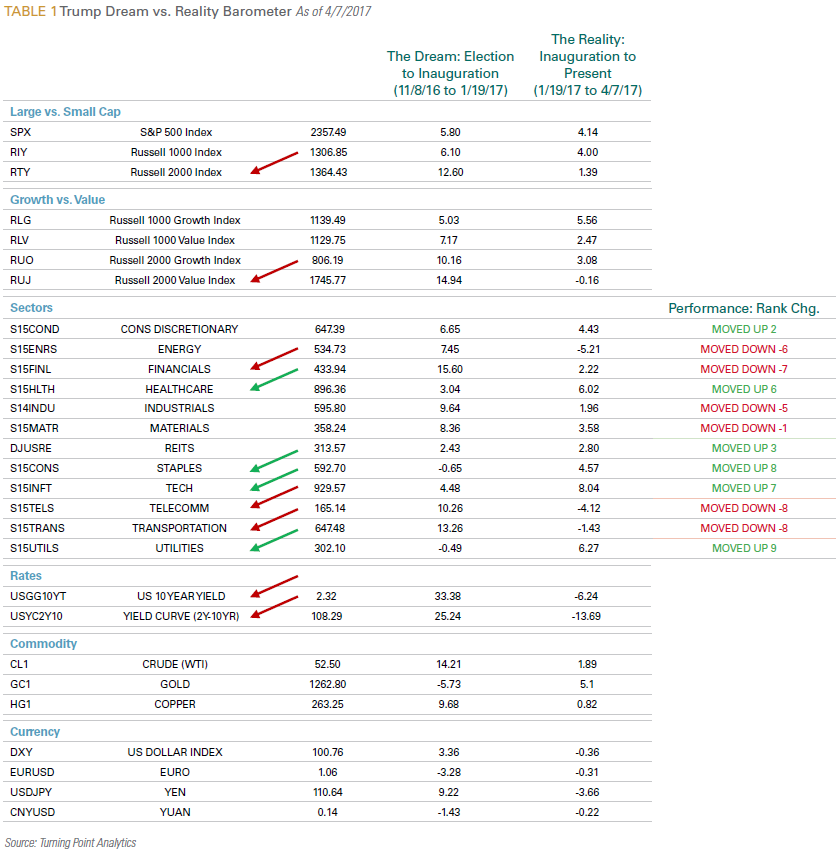

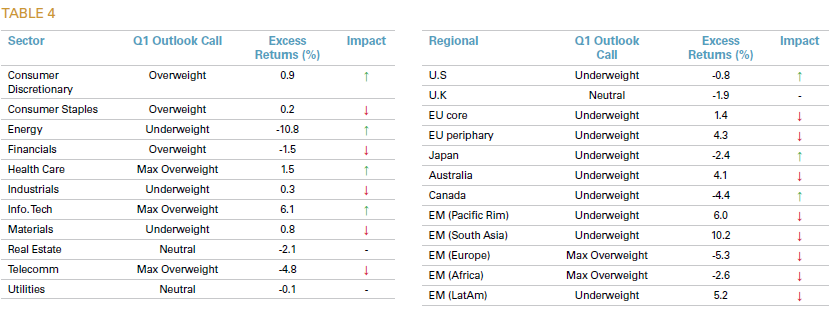

Our Q1 Outlook entitled “Who Knows? Known Unknowns and Unknown Unknowns” pinpointed risks to the seemingly unbridled bullish consensus undergirded by hopes that the Trump Administration would roll back Obamacare, financial and energy regulation and re-open fiscal spigots through a combination of tax reform and infrastructure spending. Indeed, since early March, some of the risks discussed in the paper began to challenge this consensus. Accordingly, the S&P 500 has fallen by 1.8% after hitting a record high on March 1st. Treasury yields have also backed off their highs and credit spreads have widened modestly. As shown in Table 1, many of the assumed post-election winners, such as higher tax bracket small cap stocks and financials (that would be expected to benefit from a roll-back of Dodd Frank) underperformed after the new President was inaugurated. Healthcare facilities rebounded, suggesting that many investors see failure of Obamacare replacement legislation as threatening the broader Republican agenda.

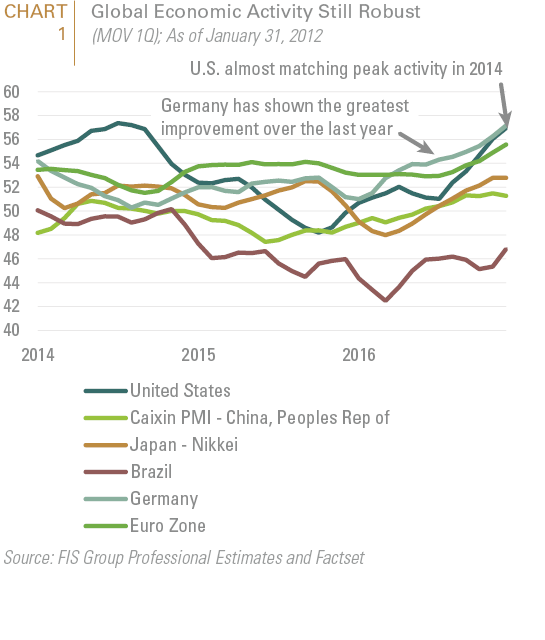

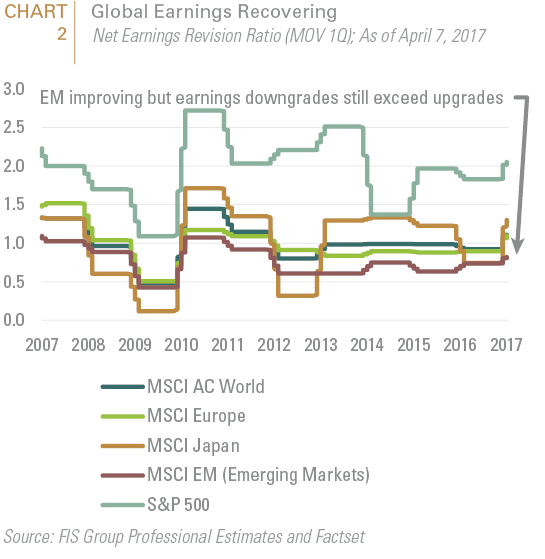

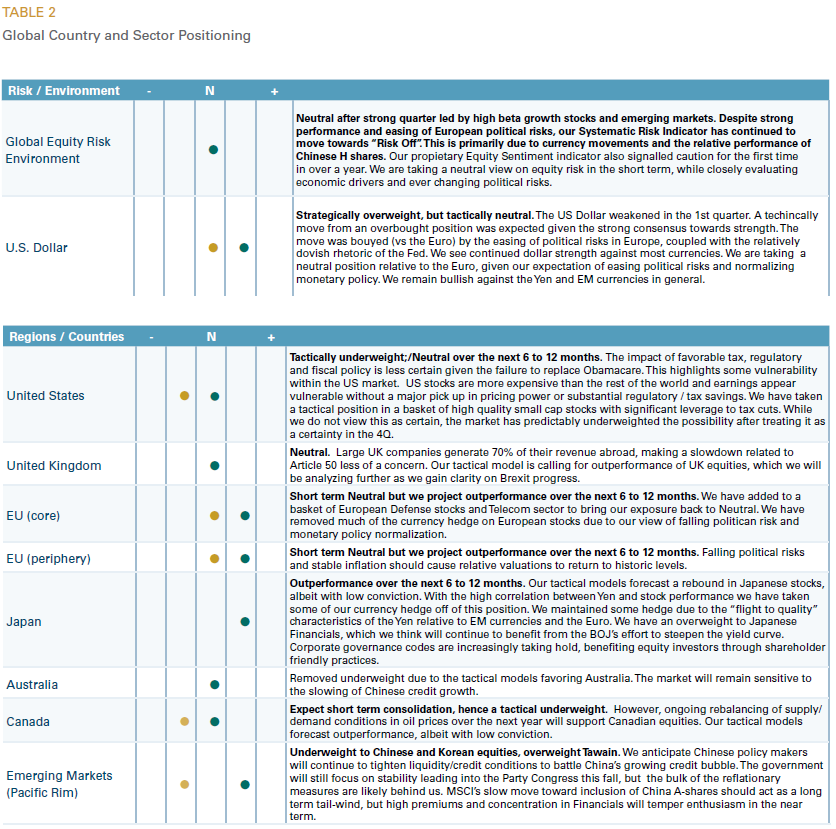

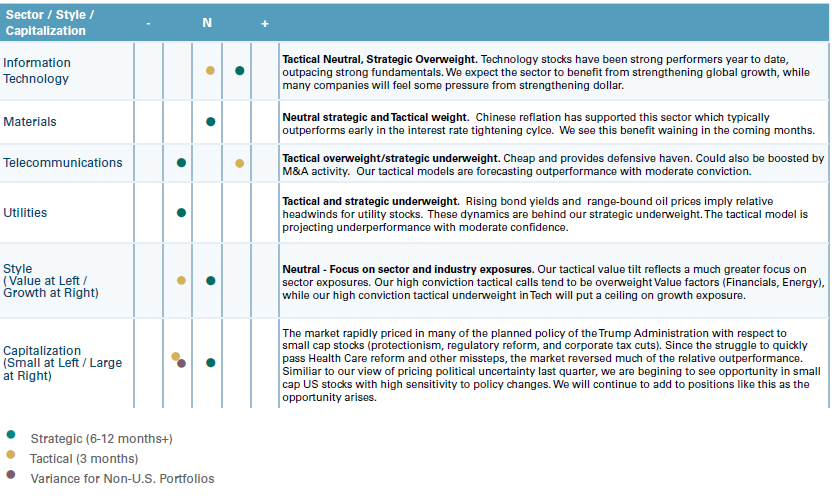

While this recent retreat in risk assets has led some investors to question the sustainability of the reflation trade, we simply view it as a pause which right-sets the overly ambitious expectations around both the scope, pace and effectiveness of the new administration’s market friendly policies. The real story is that global equities are being supported by strengthening economic data. (See Chart 1). This improving macro-economic backdrop is leading to more positive earnings revisions across the board. Indeed, only in the Emerging Markets do negative earnings revisions exceed positive revisions and even there, the ratio has been improving. (See Chart 2). For Q2, we continue to overweight European and Japanese equities at the expense of U.S. equities; while we are neutral to EM equities. Within the U.S. portfolio we are overweight value and smaller names in light of better entry points presented by their Q1 slide. Our sector positioning remains pro-cyclical, with the largest overweight in the Financial sector. However, our tactical models also call for an overweight to the more defensive Healthcare and Telecomm sectors. (Please refer to Table 2 and Table 3 below. for our sector and regional positioning). A scorecard on our Q1 positions is provided on Table 4 below. While we believe that, particularly against the Japanese Yen and commodity exposed EM currencies, the dollar bull run has more legs to go, we are reducing our hedge against the Euro which as discussed in the special section analyzing the likely path of the U.S. dollar, is the most likely candidate to stabilize against the greenback. In recognition of China’s growing importance within the Capital markets, we briefly discuss the impact of the inclusion of some China A shares in the MSCI Emerging Markets Index.

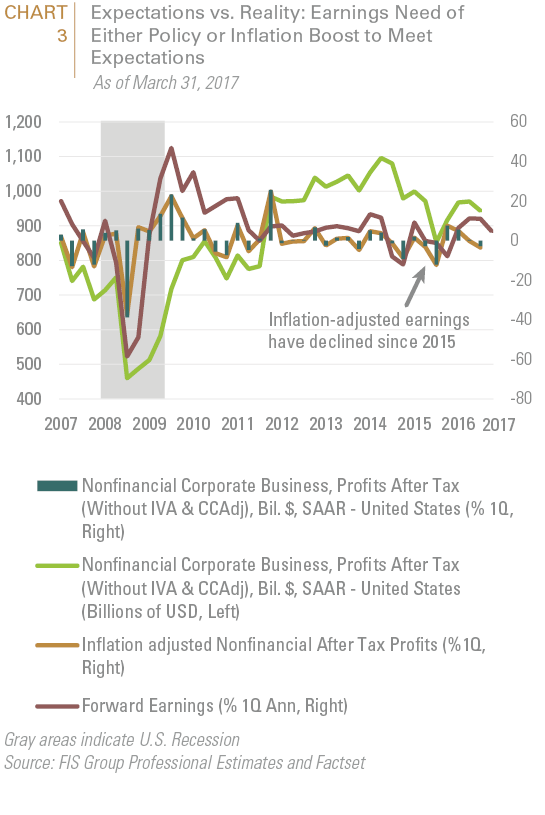

Policy expectations and synchronized global growth will continue to be the biggest themes in the market this year. In addition to being more expensive than the rest of the world, U.S. company earnings also appear vulnerable, absent a major pick-up in pricing power or a favorable policy outcome (such as corporate tax reduction). For example, Chart 3 suggests that almost all the earnings improvement last year reflected a pick-up in inflation; as profits adjusted for inflation have declined since 2015.

A recent article by the Wall Street Journal noted that while the U.S. equity market is not yet repeating the 2000 equity bubble or 2007 debt bubble, it has some of the worst features of both. For one, U.S. companies have loaded up on debt on the assumption that economic growth will continue to be slow and steady. Therefore, rather than expanding overall profit, companies have been boosting return to shareholders by replacing equity with debt. Consequently, the ratio of debt to operating cash flow of highest-quality US companies is just slightly down from a record reached last year. Secondly, while valuations are not yet at nose-bleed levels there are pockets of incredulity. The article pointed to TSLA, which is trading at a sky-high valuation justified by the hope that an untested product (in this case, mass-market electric cars) will generate big profits.

Moreover, while late cycle pricing power can lift corporate sales and margins, the corollary increase in wage pressures and interest rates can also threaten earnings, particularly considering the Trump Administration’s rhetorical pressures to dissuade American corporations from outsourcing labor to cheaper locations. As previously discussed, corporate tax reform and legislative relief would structurally support earnings. In theory, the legislative obstacles for such policies should be easier to overcome than with the controversial health care bill; but the fissures within the Republican Party suggest another protracted display of legislative wrangling and raise the probability of a less ambitious policy outcome.

The path of the U.S. dollar will also be critical in determining the year’s winners and losers. For one, currency trends will dictate how global growth is redistributed. For two, the feedback loop between the dollar and inflation could once again modify the pace at which the Fed tightens. A strong U.S. dollar, supported by perceived shifts in Fed policy, will import deflationary pressures into the U.S., undermining global-exposed sectors, such as Consumer Staples and Technology. (See Chart 4). A strong U.S. dollar is also typically negatively correlated to commodity prices and EM risk assets. For this reason, the balance of our Outlook is devoted to the U.S. dollar and its relationship with other major countries.

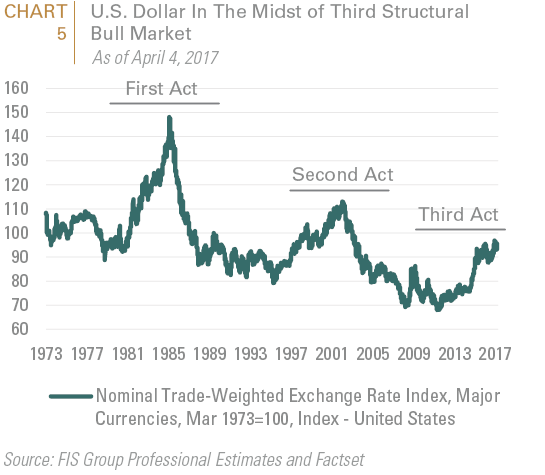

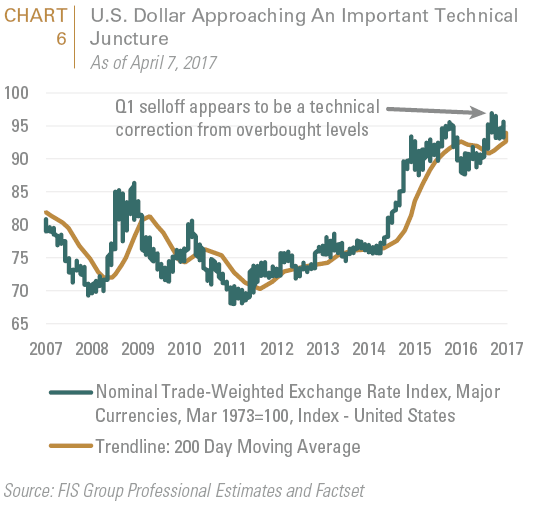

As discussed in our Q1 Outlook, there is substantial consensus that monetary policy divergence will continue to support the U.S. dollar; particularly considering that Fed continued to hike interest rates this year. We are sympathetic to this view and believe that the U.S. dollar is midway through a third secular appreciation (see Chart 5) period, supported by stronger growth in the U.S. than the rest of the world which leads to an advanced monetary policy cycle. In this context, the recent reversal partially represents a technical correction from oversold levels. As shown in Chart 6, the greenback shot well above its 200-day trend line in late 2016/early 2017 and the recent reversal has almost fully unwound this divergence.

With respect to the Japanese Yen, we believe that, absent periods of political or economic stress, the yen will continue to be challenged by policy divergence between the Fed and the BoJ. (See Chart 7).

The clear possible risk to this view is yen appreciation during periods of economic or market stress. As shown in Table 5, both the yen and the U.S. dollar are positively correlated with the Global Index of Economic Uncertainty; whereas the more pro-cyclical Euro is negatively correlated with this index.

With respect to the Euro, however, we believe that monetary policy divergence underpinning its current levels will begin to close towards the end of the year. Since inflation expectations between the U.S. and the Eurozone have remained intact since last summer, the steep divergence between bond yields and their respective currencies must therefore reflect an expectation of higher growth, at the margin, in the U.S. Alternatively, some have stated that the Euro’s depressed levels could also reflect political uncertainty emanating from the upcoming French and German elections. On both counts, we do not believe that current levels of divergence are warranted. For this reason, we are overweight European equities and have removed our U.S. dollar hedge.

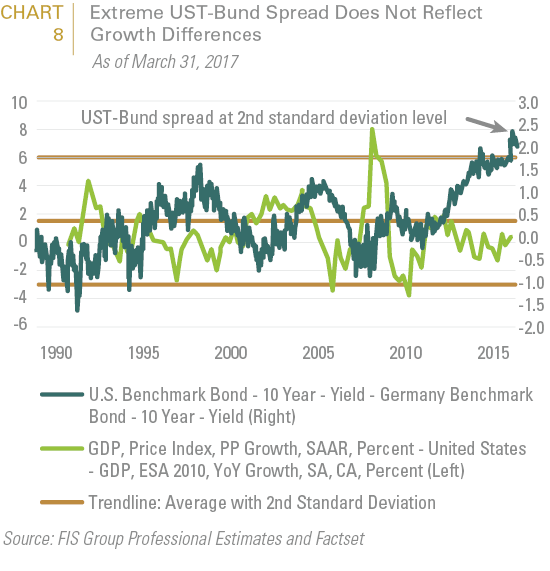

To illustrate, the spread between the U.S. Treasury bond and the German Bund is currently 2 standard deviations above its over 15-year trend. (See Chart 8). Historically, this type of deviation pushes capital flows onto U.S. shores to the point where the dollar overshoots, thus draining global liquidity until a tipping point occurs. This tipping point typically catalyzes a tactical pullback in bond prices (as well as global equity prices). The weak link this time could be emerging markets, as a sustained and unchecked dollar bull market risks uncovering the hard currency debt excesses in the region.

Chart 8 also shows that the growth differential between the U.S. and Germany is narrowing; and does not warrant the steep divergence between U.S. bond yields and German bunds. The ECB signaled at its March meeting that the Eurozone is past peak monetary policy easing with the latest 4-year TLTRO II bank take up coming in at €233bn fixed at 0%. As soon as the ECB starts to remove extraordinary monetary policy accommodation (or rather, that the markets anticipate that tapering in imminent), the UST-Bund spread should normalize and Euro will begin to stabilize. Indeed, the Euro’s appreciation last quarter was driven by market expectations of ECB tapering by the end of the year. (See Chart 9).

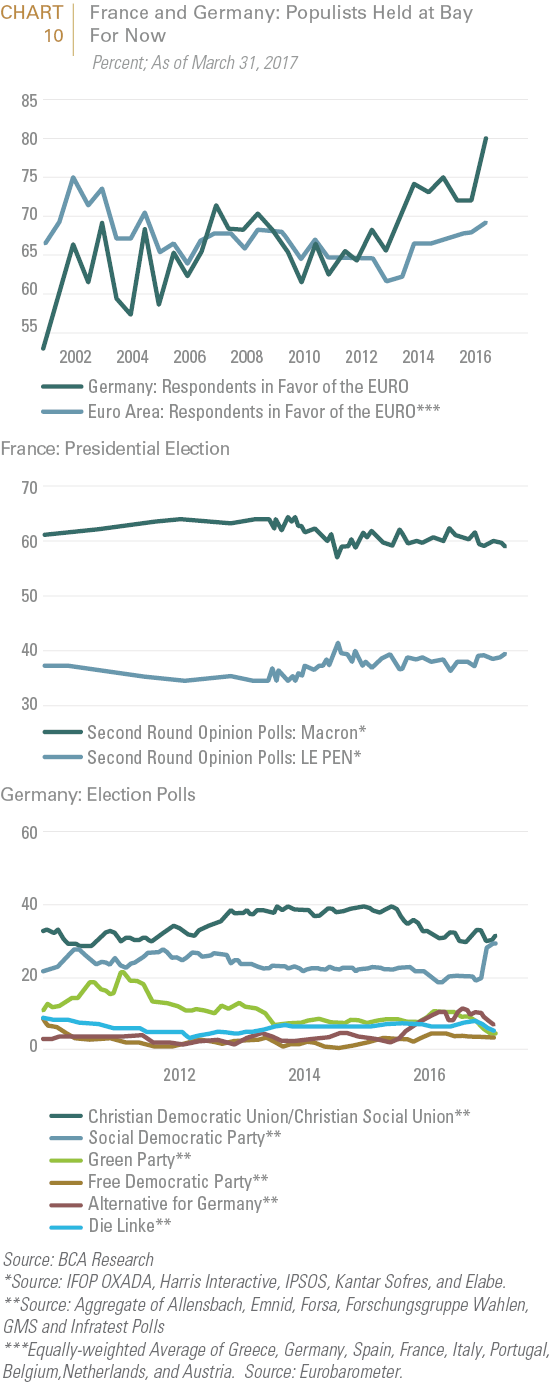

In the interim however, the ECB will likely exercise considerable caution considering imminent elections in France and Germany. Indeed, after the ECB’s chief economist Praet ignited market speculation that tapering was imminent by suggesting that changes in communication could lift long-term rates and tighten financial conditions, both ECB President Draghi and Praet more recently went to great lengths recently to assure markets that now was not the time to alter its policy stance. While they did not exclude a further reduction in the bond buying program this year, they emphasized the importance of seeing a pick-up in hard data. Since our baseline belief is that the establishment parties will prevail in both the German and French elections, (see Chart 10), we expect the Eurozone’s current economic momentum to continue. Therefore, we would not be surprised to see ECB tapering to begin in earnest in late 2017/early 2018.

EM Currencies

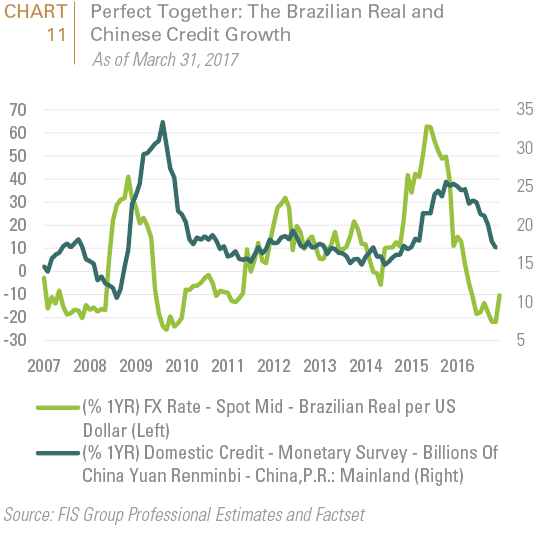

EM currencies and equity prices continued to rally in Q1 2017, aided primarily by the retracement in the U.S. dollar as well as an apparent toning down of the protectionist rhetoric which was a staple of candidate Trump. While as exhibited in Charts One and Two above, EM growth and earnings are improving, we do not believe that the greenback’s appreciation is over; nor are we convinced that some form of protectionist measures will not be implemented by a Trump Administration anxious to assuage its base. Additionally, as shown in Chart 11, EM currencies such as the Brazilian Real were boosted by rising commodity prices as a result of China’s reflation in late 2015 and 2016. In order to reign in excess credit as well as housing prices, China has been taking gradual measures to reign in credit growth. Consequently, both the number and value of newly started capital spending projects in China has waned. Over the course of 2017, this will stymie support for commodity-exposed EM curriences such as the South African Rand and the Brazilian Real.

A-share Inclusion Tiptoes Forward

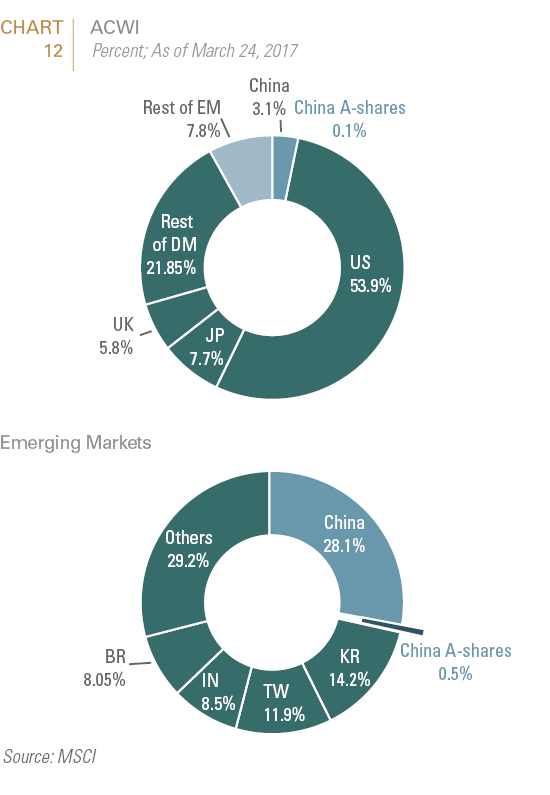

On March 24, MSCI set forth a new, and much more implementable strategy for the incremental inclusion of China A-shares into global indices. If adopted, it would result in a mere 0.5% change in the MSCI Emerging Markets index and a 0.1% change in the MSCI ACWI index (see Chart 12). As constructed, this proposal would thus not create a significant disruption in the near-term to managers and index watchers alike and so may go little noticed by the markets, especially the China A-share market where investors’ timelines are rarely measured in anything beyond months. But this proposal is critical, as it would finally put the A-shares on the long anticipated path to global index inclusion, which at full weight (which would take years) would have far-reaching ramifications for the structure of asset management in emerging markets. MSCI is presently in “consultation” about these proposed changes through June, which mostly means they are giving large investors and their other primary customers a few months to veto the idea before moving ahead. But the immensely tepid nature of this proposal seems specially designed to cater to the needs of MSCI’s principle customers, and thus gain their accession, while also balancing the urgent desires of Chinese policymakers to bring more foreign capital into their stock markets (albeit on their own terms). As such, we can envision a potential future in emerging markets equities where GEM managers as we know them today may cease to exist in a new GEM world overwhelmingly dominated by a single market. We will profile this new world in substantially more detail in a future special report this summer.

Important Disclosures:

This report is neither an offer to sell nor a solicitation to invest in any product offered by FIS Group, Inc. and should not be considered as investment advice. This report was prepared for clients and prospective clients of FIS Group and is intended to be used solely by such clients and prospects for educational and illustrative purposes. The information contained herein is proprietary to FIS Group and may not be duplicated or used for any purpose other than the educational purpose for which it has been provided. Any unauthorized use, duplication or disclosure of this report is strictly prohibited.

This report is based on information believed to be correct, but is subject to revision. Although the information provided herein has been obtained from sources which FIS Group believes to be reliable, FIS Group does not guarantee its accuracy, and such information may be incomplete or condensed. Additional information is available from FIS Group upon request.

All performance and other projections are historical and do not guarantee future performance. No assurance can be given that any particular investment objective or strategy will be achieved at a given time and actual investment results may vary over any given time.