FORESIGHT | FIS VIEWS

We are pleased to present the next ForeSights, A World Without America?, which uses a historical framework to evaluate the impact of a more insular, America First foreign policy. The investment implications of this journey will profoundly affect the risk premia attached to different assets. Therefore, we close this piece on the investment implications of an America First geopolitical policy.

At his inaugural address, President Trump touted an inward looking, “America first” foreign policy. Arguably, this posture was a stunningly explicit (and perhaps misguided) recognition of a trend that had begun with the previous administration; whose reticence to engage in military adventurism relative to his predecessors was roundly criticized by establishment hawks. Below we argue that this foreign policy trajectory is consistent with historical precedent and will greatly alter the winners and losers going forward.

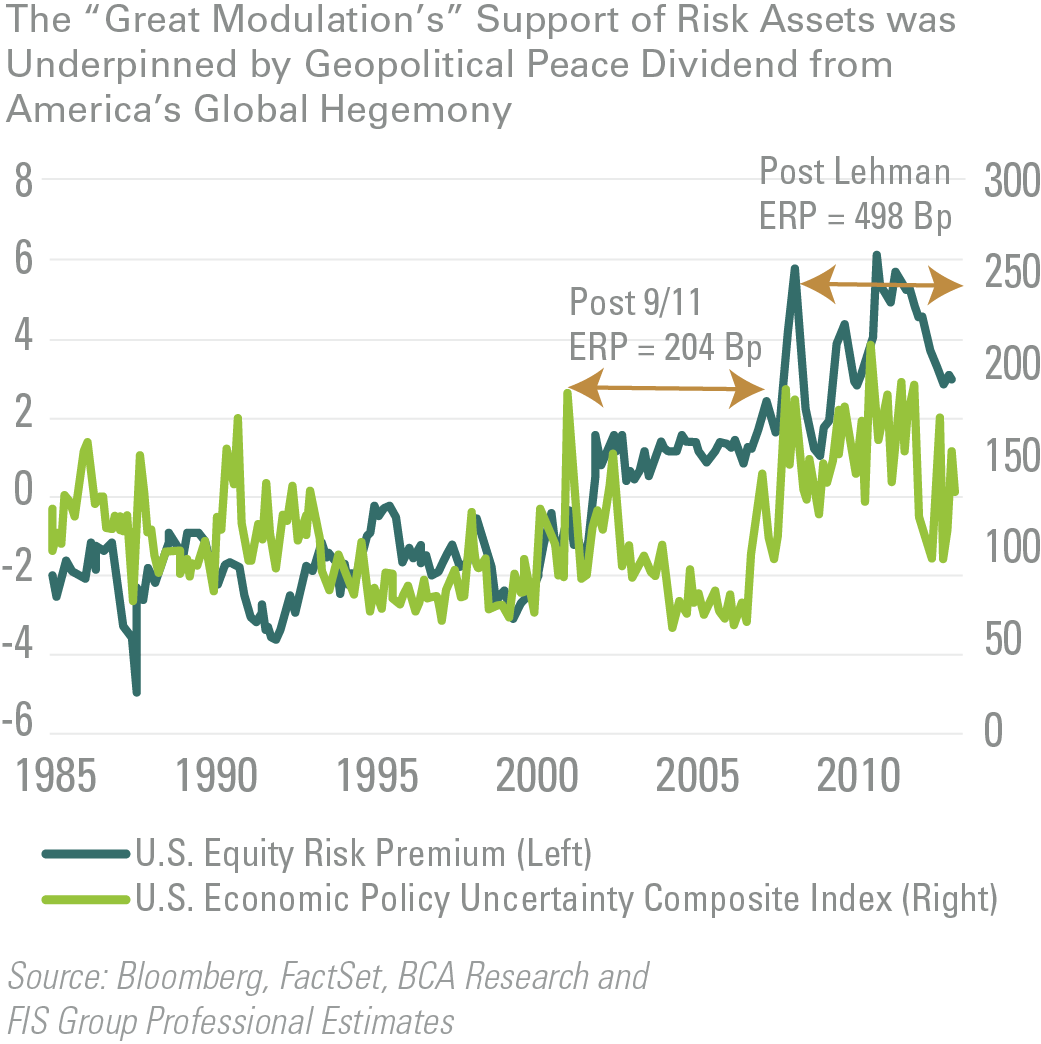

But first, why should investors care about changes in American foreign policy and more broadly, fundamental changes in the geopolitical order? We would posit that structural changes in the geopolitical landscape and world order is foundational to the long-term risk premia attached to investment assets. For example, the 30 plus year bond bull market is as much a result of the deflationary impact of trade globalization (catalyzed in particular by China’s 2001 entry into the World Trade Organization), as Fed policy. Similarly, the relatively low equity market risk premia between the end of the Cold War in 1991 and 2007 (often referred to as the “age of modulation”) was also underpinned by relative geopolitical stability. (See the chart below).

In order to understand both the historical context and long term investment implications of the current period of political tumult, we turned to the works of thinkers outside of the traditional gaggle of investment analysts, such as Thomas Freidman’s, Thank You For Being Late: An Optimist’s Guide to Thriving in the Age of Acceleration, Peter Zeihan’s The Absent Superpower and various research reports by Marko Papic, geopolitical strategist for BCA research. Each in their own way point to 3 themes:

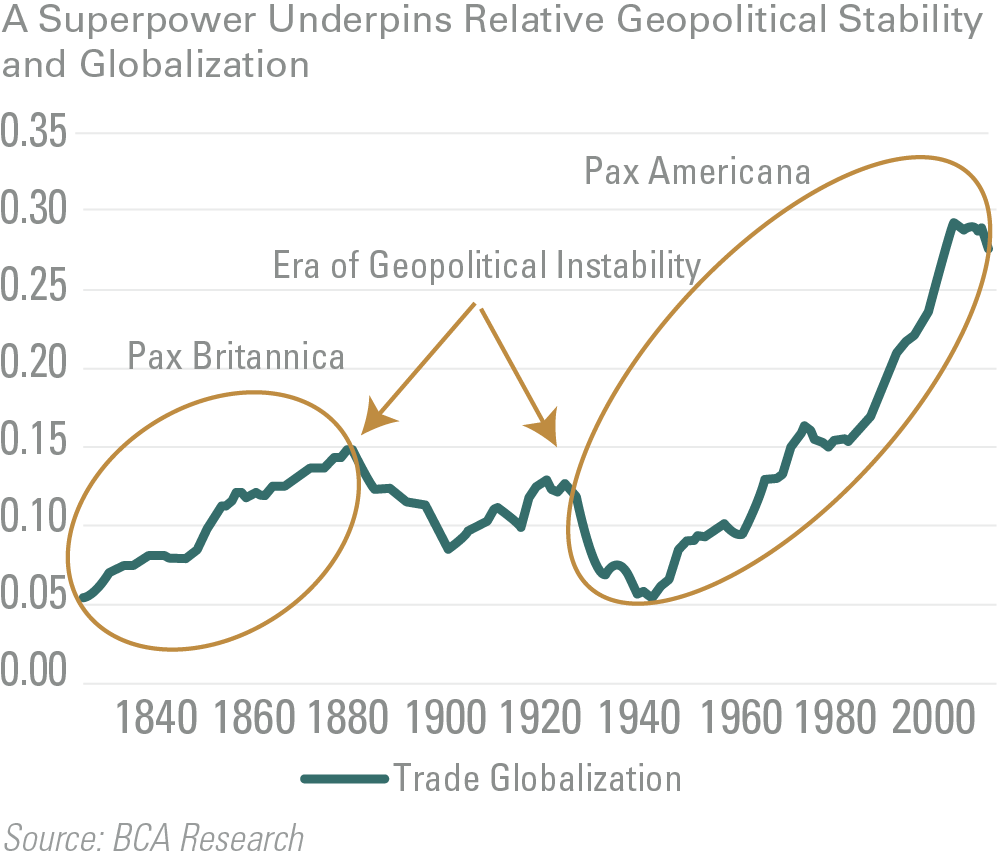

- As in the early part of the 20th century which marked the end of the 70 year reign of the British empire as the singular global hegemon, we are witnessing the closing chapters of the unparalleled 100 plus years of American hegemony. By providing expensive global public goods – such as funding international institutions, dictating global commercial arrangements and arbitrating regional disputes, securing sea lanes as well as providing the world’s reserve currency – not only did both superpowers amass heretofore unparalleled wealth and power, but they also allowed other countries to focus inwards, industrialize and eventually catch up with their hegemonic patron. Additionally, in both cases, the expenses associated with their hegemonic responsibilities as well inevitable campaigns of militaristic overreaches, exacerbated their economic decline relative to countries who were free to focus on internal development and export competitiveness under the safe harbor of relative stability provided by the hegemonic superpower. America’s upstart trade competitors have been Japan (in the 1970s and 1980s), Germany, and China. The British empire’s primary upstart competitor was Germany. The following quote from 1896 is therefore hauntingly familiar.

“The industrial glory of England is departing, and England does not know it. These are spasmodic outcries against foreign competition, but the impression they leave is fleeting and vague…German manufacturers…are undeniably superior to those produced by British houses. It is very dangerous for men to ignore facts that they the better vaunt their theories…..This is poor patriotism.”

—Earnest Edwin Williams, Made in Germany (1896)

- Both eras did not end well because for better or for worst, the diffusion of power caused by the decline of a more inwardly focused global hegemon leaves a power vacuum for other countries to assert their own regional agendas. Thus both World Wars were symptomatic of Britain’s decline as the only superpower which mattered. Today, Russia’s increasing aggression to reassert its regional hegemony over its former vassal states; China’s assertions in the South China Sea and Japan’s consequent efforts to re-militarize; as well as Saudi Arabia and Iran’s competition for regional hegemony are all symptomatic of controlled fissures that have re-erupted as a result of their increasing geopolitical significance or insecurity as well as America’s relative retreat from being the global policeman to a more insular focus. America’s inward pivot will not only expose poorly governed and uncompetitive nation states that were propped up by its (and during the Cold War, Russia’s) competition for geopolitical control, but it will destabilize the current world order (as each nation would need to bear more of the burden for their own economic, social and geopolitical security). Geopolitical uncertainty increases because the world transitions from one of relative cooperation under the rules and institutions imposed by the superpower (such as the WTO, NATO, the IMF and the World Bank) to a less stable zero sum order. This period of instability will continue until a new hegemonic nation state or states arise and impose their rules and institutions (perhaps China or a combination of the US and China?).

- The relative decline in both superpower hegemons led to increased geopolitical instability and a retreat in trade globalization. (See the chart below).

In some ways, a retreat to a more mercantilist world benefits those countries that are least dependent on trade for their economic survival. In this regard, the relatively insular American economy, where exports represent only 12% of GDP, and is protected by its geographical isolation would be least vulnerable in such an environment.

However, Friedman in particular argues that the retreat in traditional trade of goods and services is and will continue to be vastly superseded by digital interconnectivity. So while the world grows more mercantilist in terms of the traditional trading of goods and services, it will flatten and become more interconnected, despite the attempts of policy makers to erect or reinforce national boundaries and trade protections. For example, according to the 2013 McKinsey Digital Flows study, back in 1990, “the total value of global flows of goods, services, and finance amounted to $ 5 trillion, or 24 percent of world GDP. The public Internet was in its infancy. Fast-forward to 2014: some $ 30 trillion worth of goods, services, and finance, equivalent to 39 percent of GDP, was exchanged across the world’s borders.” Cross-border bandwidth [terabits per second] has grown 45 times larger since 2005 and is projected to grow by another nine times in the next five years as digital flows of commerce, information, searches, video, communication, and intra-company traffic continue to surge.

This phenomenon will change the calculus of winners and losers away from countries and organizations that control the greatest “stock” of physical resources on which they can impose economic rents, to those who control and harness the greatest amount of digital “flows” of information and technological innovations. On a micro level, think of the difference between traditional media companies and Facebook, whose digital reach has propelled what started out as mere social interaction platform to arguably, one of the most influential media companies globally. On a country level, the Obama Administration’s “pivot” away from the Middle East was accommodated by technological innovations in fracking, horizontal mining as well as renewable energy which lessened America’s dependence on oil from the Middle East. This pivot along with lower oil prices ushered in by the increased global energy supply has in essence, defanged OPEC as the monopoly price setter, made Gulf oil producers (who relied on high oil prices for imposing domestic social stability and American oil dependence for geopolitical protection) more vulnerable; which in turn has ratcheted up regional Middle East tensions.

Freidman would probably also challenge Freihan’s assumptions around the primacy of the protections that arise from America’s geographical isolation. One need only to look at new modes of warfare, such as cyberattacks and drone technology to understand that the game has shifted. Global interconnectedness, also leaves all countries and financial markets more vulnerable to less powerful bad actors.

Conclusion and Investment Themes

From an investment point of view, a few themes come to mind as likely to do well in the evolving world order. These themes are in large part similar to those expressed in our Q1 2017 Outlook:

- America First!: while demanding equity valuations for US equities relative to other regions make them less attractive for the intermediate period, as mentioned previously, a more mercantilist world should benefit the large and more domestically powered U.S. economy. Additionally, America, like Switzerland, is a relatively low beta market which typically outperforms in times of geopolitical uncertainty. This is in part why Zeihan and Papic believe that the next decade will belong to America. On the other hand, highly trade dependent countries such as the Asian tiger countries and much of the Emerging World that benefited from globalization would be expected to underperform. However, within the emerging world, countries whose economy are more domestically driven, such as India, would be least vulnerable. A significant risk to this theme is that America’s assets not only comprise of its large domestic economy and geographical isolation, but also its technological innovation fostered by its educational institutions, its attractiveness to bright and entrepreneurial minds all over the world (according to the American Enterprise Institute, despite representing around 10% of population, 40% of America’s Fortune 500 companies were founded by immigrants or their children) as well its laissez faire creative destruction. It is these features that have allowed America to dominate the rapidly expanding digital economy. To the extent that federal policy undermines these attributes, America will be weakened.

- Investors should re-acquaint themselves with higher risk premia and a greater likelihood and frequency of left-tail risk events catalyzed by an uptick in geopolitical instability. The combination of more interconnected global markets and the increasing market relevance of algorithmic funds and high frequency trading strategies could amplify such events. This is because many of these strategies embed similar algorithms that tend to close their positions when market volatility increases. To the degree that their positions are highly levered (which is a worrying unknown at a total market level), these strategies could become the epicenter of a systemic market shock.

- US Small Cap over Large Cap: The conflicts will stall global trade, so companies with predominantly domestic revenues should be better positioned than companies with global sales. Historically, small cap stocks fit that bill.

- Energy: The structure of the oil market has changed. In the 1970s, and even up to the early 2000s—the OPEC cartel agreed to production quotas in order to defend the market shares of its members. The approach worked because the principal competition was among oil producers, and in particular between Opec and non-Opec producers. Today, the biggest competitive threat to any one oil producer is not other producers, but alternative sources of energy. These alternative sources have become the marginal price setters. Therefore the trading range of oil will be capped at the marginal cost of shale production (currently around $60/bbl). That said, instability in the Middle East will add a geopolitical premium to oil and natural gas prices. This should be particularly profitable for the American shale industry.

- Defense: This one is the highest conviction calls from our January outlook. A more unstable world will have more conflicts; armies will need to buy their weapons from someone. Cyber defense companies will also outperform.

- Increasing Inflation. Globalization is inherently deflationary as it allows corporations to source labor and resources from the most inexpensive sources. Therefore, a retreat from globalization will stem the deflationary impulse which has suppressed global bond yields and underpinned the 30 plus year bond bull market. This should support inflation sensitive real assets, such as real estate, infrastructure and gold; which has the added benefit of being a safety asset.

- Declining profit margins. Globalization expanded sales and reduced costs; which shifted the economic pie towards corporate profits and away from labor in developed countries. Therefore, a more mercantilist world would be expected to reverse this trend.

This report is neither an offer to sell nor a solicitation to invest in any product offered by FIS Group, Inc. and should not be considered as investment advice. This report was prepared for clients and prospective clients of FIS Group and is intended to be used solely by such clients and prospects for educational and illustrative purposes. The information contained herein is proprietary to FIS Group and may not be duplicated or used for any purpose other than the educational purpose for which it has been provided. Any unauthorized use, duplication or disclosure of this report is strictly prohibited.

This report is based on information believed to be correct, but is subject to revision. Although the information provided herein has been obtained from sources which FIS Group believes to be reliable, FIS Group does not guarantee its accuracy, and such information may be incomplete or condensed. Additional information is available from FIS Group upon request.

All performance and other projections are historical and do not guarantee future performance. No assurance can be given that any particular investment objective or strategy will be achieved at a given time and actual investment results may vary over any given time.