FIS Group has focused on sourcing and evaluating small boutique managers, including minority and women-owned firms, for over 21 years. Our research product includes monitoring the industry environment, and how it impacts these firms.

The Markets in Financial Directive (“MiFID”), set to be enacted in early 2018, will regulate how asset managers pay for the research they utilize in making investment decisions. While the proposed MiFID II regulatory changes are well-meaning, we believe they represent yet another costly regulation that could have a disproportionately negative impact on small firms as opposed to large ones.

Amid the relentless migration of institutional asset to mega-sized firms, this move could imperil small managers, and increase potential systemic risk in the marketplace. We discuss the backdrop for this regulatory change and the specific potential impact on emerging managers in detail in this FIS Market Insights Alert.

The Markets in Financial Directive (“MiFID”) is a European Union law that provides harmonized regulation for investment services across the 31 member states of the European Economic Area (the 28 EU member states plus Iceland, Norway and Liechtenstein). MiFID II, the amended law which goes into effect in January 2018, stems from regulation that European Union law makers enacted to regulate how asset managers pay for the research they utilize in making investment decisions. This regulation has good intentions and the primary benefits are:

- It creates more transparency for clients

- It transfers the cost of research from clients (in the form of trade commissions) to the manager (if the manager doesn’t pass this cost back to the client)

MiFID II only applies to European firms, but recently a significant amount of large brokerage houses and asset managers seem to be adopting the regulations on a global scale, which we believe will transform expectations on how investment managers should allocate and report their expenses incurred for securities research. The purpose of this research note is to evaluate the impact of these changes on boutique or smaller entrepreneurial investment managers.

Investment managers have traditionally used trading commissions generated through their portfolio trading, or so called “soft dollars”, to pay for research. A late 2016 MiFID II discussion paper by PWC implied that security or sector based research, economic insight, access to company executive management on roadshows, analyst conferences, and excel company models can all be considered research products that will have a cost attached. Basically, almost everything that brokerage firms’ offer will become a cost for managers. Additionally, based on recently published articles, most brokerage firms are being conservative in their approach and are indicating that they plan on charging for a majority of their research in order to avoid the administrative and regulatory burdens of maintaining two pricing models.

At FIS we globally source, evaluate, and retain smaller/entreprenuerial managers because of their greater flexibility to identify alpha opportunities across the capitalization spectrum and their ability to trade more nimbly, particularly in less liquid markets. While this ruling creates much needed transparency in manager expense reporting, it could present yet another headwind for smaller/entreprenuerial managers for whom third-party fundamental stock research is integral to portfolio management.

In summary, we believe that widespread adoption of MiFID II, while well-meaning in its facilitation of greater transparency on research expenses, represents yet another regulation whose costs will be disproportionately borne by smaller, fundamentally driven investment boutiques, and thus will further exacerbate the increasing concentration of investment assets towards very large firms. Therefore, we expect further declines in new firm formation, as well as more firm closures and/or further consolidations/collaborations among small investment boutiques to leverage operational synergies.

MiFID II’s Impact

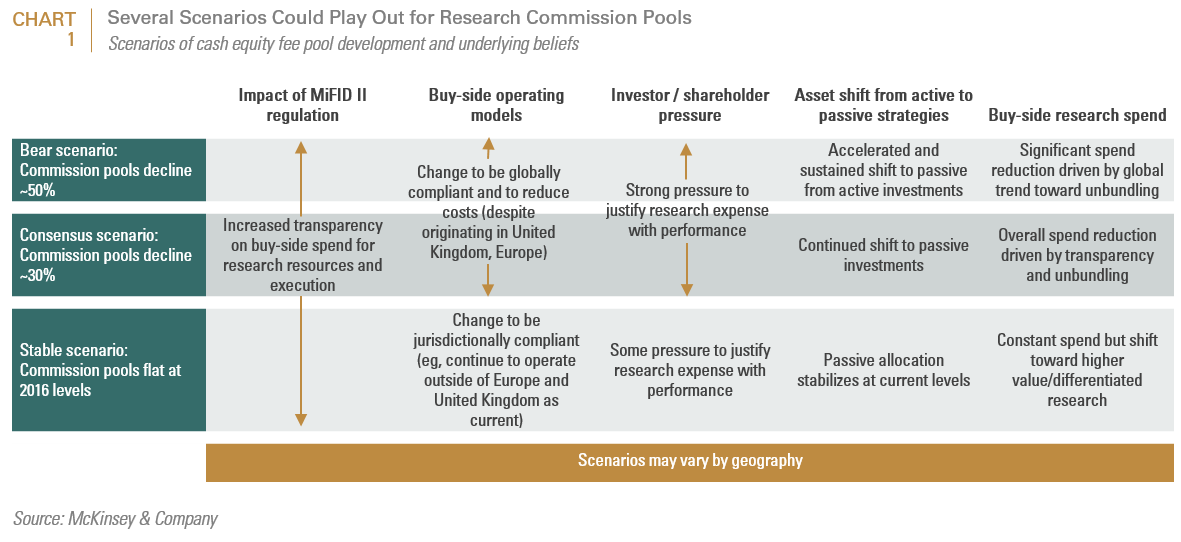

Recently, McKinsey & Company wrote a paper entitled “Reinventing equity research as a profit-making business”, which provided the diagram (on the next page) to delineate the potential outcomes from the upcoming MiFID II rule changes. As the diagram shows, in a Bear scenario, one could see an overall commission revenues decline of 50%; due to what they posit could be a second-order impact of MiFID II – further asset migration away from actively managed strategies because of investor pressure to justify now more transparent research expenses during periods of challenged active manager performance. Even the Consensus strategy is estimated by the report to result in a commission decline of 30% as active managers are driven to reduce research costs, and justify their reduced spend (see Chart 1).

For smaller managers, soft dollar arrangements with brokerage firms allow them to defray the cost of securities research. However, through MIFID II, even US based managers will be affected because brokerage houses are unlikely to offer two pricing models for their research. Financial Times recently published an article stating that Credit Agricole(starting cost €60K), Nomura ($134K for premium), Deutche Bank AG ($35K for 10 people), Bank of America ML (premium package priced around $100K) and even JP Morgan would be moving to one pricing structure. Some US based firms such as Goldman Sachs have not made a definite decision yet. Should this occur, investment managers will need to add research as a budgeted line item and could face higher compliance costs (as their in-house proprietary systems might not be suitable for the MiFID reporting requirements).

Moreover, smaller boutique or entrepreneurial firms’ operating margins are already being squeezed by higher cost structures from both regulation and distribution (as individuals and international allocators overtake U.S. defined benefit plans as a source of new organic growth) and slowing revenues because of the relentless competition and downward fee pressures arising from passive strategies. Additionally, with so called “hard-dollar” research transparency, compliance costs could possibly increase because now research will need to be properly vetted, disclosed, and retained since it is an input to the investment process. In such a precarious operating environment MiFID II, while well intentioned, may be the final straw for firms struggling to survive. The Financial Times pointed out in an 8/23 article entitled MiFID II rules on research payments will harm investment boutiques:

“The direction of MiFID II, whether intended or not, clearly favors larger fund companies who can pay for research from their significant commissions budgets, which further raises the barriers for entrants to the investment industry.”

For allocators watching the rules change, MiFID II could also create an industry shakeout that should provide managers with competitive performance and strong balance sheets the opportunity to stand out. This change, as noted above, could also tip the scales towards quantitative strategies that are less dependent on third-party fundamental research.

Our Takeaways

It is possible that if brokerages start charging for “hard dollars” for research, this regulation will further enhance the competitive advantage of large firms whose balance sheets can better weather higher research expenses. Additionally, systematic or quantitative managers or managers whose security selection is entirely or primarily derived from internal research, will be somewhat shielded from MiFID II’s impact.

On the positive side, the need to pay “hard dollars” will raise the bar for the quality of research and could increase the demand for more niche research firms, along with research exchanges. It is not far-fetched to imagine more firms concentrating on industry/sector specific or market cap biased research, with an emphasis on unique and more thorough analysis, since resources on the buyside will become compressed. This should create a need for better sell-side analysts along with improved industry models. It could also lead to more subscription based platforms that allow access to freelance research where star analysts’ reports are accessed through research exchanges. Ultimately, regulations such as MiFID II will hasten the adoption by forward thinking firms of technology based research services, such as sensing and artificial intelligence, which we believe will substantially drive down the cost of research. While enhancing operational efficiency, technology-based and/or less expensive off-shore research solutions could, however, diminish job opportunities for research analysts which have been an important source of future portfolio managers.

In an already challenging operating environment, this new regulation could further challenge boutique small/entrepreneurial managers. Earlier this year the Tabb Group noted that 76% of the US Managers surveyed by them would fall under some MiFID II rules. Based on a survey of the boutique (sub-2 billion dollars in AUM) managers in our database, about 20% utilize soft dollars and sell side research. This lower number could reflect FIS’ bias towards managers whose security selection is primarily based on proprietary research. However, it also reflects the fact that most of the managers surveyed are U.S. domiciled and do not have non-U.S. clients. For example, managers in our database that are domiciled outside of the U.S. almost universally stated that MiFID II could present an operational challenge. This would suggest, that should brokerage houses adopt a uniform pricing structure which conforms with MiFID II, then their U.S. peers would obviously feel less insulated from its impact.

This report is neither an offer to sell nor a solicitation to invest in any product offered by FIS Group, Inc. and should not be considered as investment advice. This report was prepared for clients and prospective clients of FIS Group and is intended to be used solely by such clients and prospects for educational and illustrative purposes. The information contained herein is proprietary to FIS Group and may not be duplicated or used for any purpose other than the educational purpose for which it has been provided. Any unauthorized use, duplication or disclosure of this report is strictly prohibited.

This report is based on information believed to be correct, but is subject to revision. Although the information provided herein has been obtained from sources which FIS Group believes to be reliable, FIS Group does not guarantee its accuracy, and such information may be incomplete or condensed. Additional information is available from FIS Group upon request.

All performance and other projections are historical and do not guarantee future performance. No assurance can be given that any particular investment objective or strategy will be achieved at a given time and actual investment results may vary over any given time.