Article Summary

This Alert highlights FIS Group’s views on the investment implications of Trump’s current proposed policy intentions, such as:

1. A delay in the anticipated Fed hike in December due to continued market turmoil;

2. Industrial stocks benefiting from increased infrastructure and defense spending;

3. Financial stocks benefiting from increased rates and the paring back of Dodd-Frank regulations;

4. A steeper yield curve that would boost value oriented stocks relative to bond proxies and growth stocks;

5. Bio-tech and pharmaceutical companies expected to face less pricing pressures if the Affordable Care Act is repealed with the backing of an all-Republican Congress;

6. A decrease in M&A activity with insurance companies and less stress on the liquidity of their surplus accounts; and

7. A shift in policy choices that would significantly impact trade, wage and profit growth thus changing the line-up of winning and losing economic agents and investments.

Donald Trump’s unexpected victory in the U.S. presidential elections was another resounding expression of the phenomenon which we described as The Revenge of the Precariat over Davos Man in our July post Brexit commentary.1 Trump, like his British counterparts, eschewed long held political and policy assumptions and stitched together a new coalition bound by disaffection with rapid changes in our societal makeup and economic opportunity; as well as a generalized anger at a “system” from which they feel increasingly disconnected. In the U.S., this disaffection is best demonstrated by increasing pessimism about the future at the dawn of the 21st century. For example, an August 2014 Washington Post article reported that when asked if “life for our children’s generation will be better than it has been for us”, 76% of U.S. respondents did not have such confidence; compared to 43% in 2001.

In light of the global financial crisis’ (GFC) erosion of public confidence in our political and financial institutions, as well as anemic growth that has followed it, the current surge in populism in the U.S. and Europe is unsurprising. Thus, in addition to Brexit and the U.S., in Italy, the world’s fourth largest sovereign debt market, comedian Beppe Grillo’s Five Star Movement is neck-and-neck in the polls with the status quo governing Democratic Party. In France, nationalist and ardent Eurosceptic Marine Le Pen will likely enter the final round of the May 2017 presidential election (though she is unlikely to win).

As with Brexit, professional pollsters completely underestimated the mood of the electorate (or perhaps, those polled were not straightforward about their preference for the controversial Mr. Trump) and almost universally predicted a Clinton win. In both the U.K. and the U.S., the starting premise of the political establishment, dominated by the Davos class, was that elections are decided by core middle class voters who are averse to economic risk and allergic to radical lurches (towards the left or right), in spite of their anxieties. Similarly, in the US, based on the frequency with which it was aired, the campaign advertisement that was considered most post potent recounted Trump’s many ill-tempered pronouncements while declaring Hillary Clinton as the stable and safe alternative.

So far, Precariat’s “leaders” have not emerged from their own ranks. After all, Brexit leaders, such as Michael Gove and former London Mayor Boris Johnson are both Oxford Men. While Mr. Trump bills himself as a political outsider, he is hardly Precariat. However, these men have profited from a similar play book: sew distrust with the political and financial establishment; cynical manipulation of national and racial attachments by objectifying minorities and immigrants, and vague promises to bring back jobs that have been savaged by trade (their favorite chimera) and technological advancement (which was rarely, if ever, discussed).

As discussed in our Q4 2016 Outlook, at bottom, the current angst among many voters has been spurred by insufficient economic growth – in that there’s simply not enough of it to keep everybody happy while paying the debt and entitlements we have promised ourselves in old age. Even before the GFC, prosperity had bypassed the Precariats in that 21st century corporate giants, such as Facebook and Apple are far less labor intensive than their counterparts in 1950’s and 60’s, such as GM and Xerox, that propelled millions of the Precariat into the middle class. Many of their jobs have been replaced by technology, and increasing globalization led to a shift of income from low-skilled workers to high-skilled workers. Moreover, the increasing integration of the global labor market between rich and poor countries has effectively given companies in rich countries access to a large new pool of workers, thereby increasing corporate profits which disproportionately favored the financial Davos elite. These trends resulted in an overall decrease in the share of national income going to Precariat labor and a rising income inequality. Furthermore, immigration has hit low skilled workers the hardest, given that approximately 28% of foreign-born workers in the U.S. do not have a high school diploma, which puts them into direct competition with less skilled domestic labor. After the GFC, the Precariat were especially peeved at the apparent immunity of the elite from any consequences of their prior mismanagement that led to the financial crisis.

In the United States and China, the world’s manufacturing powerhouses, fewer people work in manufacturing today than in 1997, thanks at least in part to automation. Modern automotive plants, many of which were transformed by industrial robotics in the 1980s, routinely use machines that autonomously weld and paint body parts—tasks that were once handled by humans. Research by MIT economist David Ator shows that between 1980 and 2005, the middle class suffered both in share of jobs and in wage growth. Since the 1980s, Ator posits that computers have increasingly taken over such tasks as bookkeeping, clerical work, and repetitive production jobs in manufacturing—all of which typically provided middle-class pay. At the same time, higher-paying jobs requiring creativity and problem-solving skills, often aided by computers and low-skilled jobs, (such as restaurant workers, janitors, home health aides, and others doing service work that is nearly impossible to automate), have proliferated. The result, according to Autor, has been an apparent “polarization” of the workforce and a “hollowing out” of the middle class—something that has been happening in numerous industrialized countries for the last several decades. This is why post-election surveys of Trump voters show a preponderance of middle income earners as opposed to the popular narrative of down-in their luck workers; because they have borne the brunt of technological disruption. The trouble is that this disruption is accelerating, as some robots already cost less to operate than the salaries of the humans they replace, and they are getting cheaper and better. For example, Boston Consulting Group predicts that, by 2025, the operating cost of a robot that does welding will be less than $2 per hour. That’s more affordable than the $25 per hour that a human welder earns today in the U.S., and even cheaper than the pay of skilled workers in the lowest-income countries. Machines are, learning to do the jobs of manufacturing workers; artificial intelligence-based tools are mastering the jobs of call-center and knowledge workers; and cars are beginning to drive themselves. Over the next decade, technology will decimate more jobs in many professions, inequality will increase. So, the real question is even if Trump and his trans-Atlantic cohorts make good on their promise to keep immigrants out, how will they stop the advance of robots?

Now that they are prevailing, it is our hope that these self-appointed representatives of the Precariat will use the anger that they have clearly tapped into as fuel for progress; and not squander it by continuing to flirt with uncontrolled institutional and economic arson. While we are somewhat troubled by the absence of substantive policy prescriptions, as we have written before in the July paper; Trump and his trans-Atlantic cohorts have tapped into a real vein of economic dislocation and feeling of abandonment which is laid most bare in the so-called “Rust belt” of the U.S. and the northern industrial section of the U.K. Therefore, we also hope that the Davos elite will turn their considerable resources to address the grievances that underlie what they have too often dismissed as nothing more than the whining reminiscences of xenophobic “bumpkins”. In doing so, we hope to see policies which raise employment and boost wages, because while “unconventional” monetary policies have been effective in stemming liquidity crises and propping up investment account balances through the so called “wealth effect”; they are not designed to expand aggregate demand in the real economy in which the Precariat primarily preside. Moreover, some central banks like the BoJ appear to have reached the point at which monetary policy may be doing more harm than good. Fiscal spending through infrastructure would be more effective for expanding aggregate demand, even though its impact will be lagged. Such policies could also help break the deflationary malaise plaguing the global economy. For example, the IMF and others have found that the shift in income from poorer to richer households, along with a falling share of national income going to labor, has depressed US aggregate demand by about 3% of GDP since the late 1970s. However, the most critical long term solution is to address the significant displacement caused by globalization with skills retraining and educational curricula that equip our citizenry for 21st century jobs. This is why the best predictor for both Brexit and Trump support was level of education, suggesting that the Precariat ultimately decided based on their own personal level of competitiveness in a globalized economy.

Investment Implications

As with the aftermath of Brexit, US equity markets initially responded negatively to the political uncertainty of a Trump win but appeared to once again finding its sea legs towards to the close of the markets on November 9th, particularly after Mr. Trump seemed to convey a more measured tone.

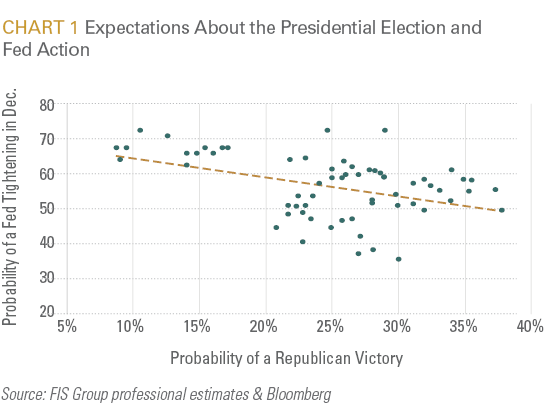

Continued market turmoil could also delay the Fed hike which widely anticipated in December. The chart below appears to depict a clear negative correlation between a Trump win and the likelihood of a December rate hike.

While Chair Yellen’s term does not end until February 2018, Trump has made no secret for his distaste for her “lower for longer” policy; which could potentially change the make-up of the FOMC. This of course could be very unsettling for the markets.

Trump’s somewhat fluid ideology renders any prognostications on the investment implications of his presidency (including ours) somewhat tenuous. Therefore the analysis below focuses on measures that he has repeatedly put forward as policy intentions.

For example, with the Republicans controlling both houses of Congress, Trump’s fiscal plans are more likely to be adopted. Candidate Trump’s proposal to couple increased infrastructure and defense spending should obviously benefit certain industrial stocks. However, his additional promise of massive tax cuts that could amount to $6trn over the next decade, would be expected to widen the budget deficit and place the Federal debt on a path to exceed 100% of GDP within the next 3 years. Consequently, while these policies would increase aggregate demand (albeit with a lag), they would also be expected to raise rates, boost inflation and close the curtain on the 30 plus year bond bull market. Increased rates, particularly if coupled with a paring back of Dodd-Frank regulations, would benefit financial stocks. As rates rise, clean balance sheets also become increasingly important. Overleveraged firms will be forced to refinance at increasingly higher rates. Favor high quality firms. More broadly, a steeper yield curve would be expected to boost value oriented stocks relative to bond proxies and growth stocks.

Additionally, should Trump’s pledge to repeal the Affordable Care Act with the backing of an all-Republican congress occur, bio-tech and pharmaceutical companies would be expected to face less pricing pressures. Insurance companies will also be affected if Trump and the Congress repeal the ACA as this would possibly put a halt on M&A activities as firms would be back to status quo before the law was enacted, which would allow smaller/mid-tier firms to be more competitive. The change would also put less stress on the liquidity of their surplus accounts as Insurance Funds would no longer be forced to float payments to the government that could take up to a year and a half to receive payment. This release in funds would allow them to increase their duration and illiquidity risk within their surplus portfolios.

We firmly believe that the underlying drivers of voter resentment will materially shift policy choices which could significantly impact trade, wage and profit growth. This will in turn change the line-up of winning and losing economic agents and investments. For example, Trump’s promise to withdraw from or renegotiate trade deals or label China as a currency manipulator could spur retaliatory protectionist measures. Since global integration has already occurred, we believe that closing the doors to foreign trade is at this point unlikely to restore the same type of jobs that were lost in the wake of much maligned trade pacts, such as NAFTA; but will more likely slow the global economy and hurt American exports, thereby shrinking the U.S. economy and accelerating job loss. Moreover, since wages have begun to rise in China and import tariffs globally have been quite low for over the last two decades, both the benefits and the costs of global trade have in effect diminished. Additionally, rising protectionism and reduced global cooperation would also be expected to escalate the armaments race, which would support defense stocks. Multinational companies that have benefitted from new markets as well as the ability to source lower labor and input costs globally, would be expected to be negatively impacted by protectionist policies. One would also expect large cap companies whose operating profits are more leveraged to globalization to underperform more domestically exposed small cap companies. Additionally, countries that are most exposed to trade with the U.S. (such as Mexico and Canada) would likely be challenged, as would export oriented EM economies, such as Taiwan and Korea.

Trump’s promise to cancel the Paris Climate Change Accord and general hostility to climate change measures would hardly be supportive of renewable energy sectors such as solar and wind. That said, from a longer-term perspective, delays in adopting measures to arrest Global Warming would be expected to put further pressure on property and casualty insurers as well as coastal areas.

In combination, increased protectionism and fiscal expansion would in combination, be expected to increase inflation. Investment assets that we would expect to outperform from such dynamics include Japanese equities (on a currency hedged basis), real assets and precious metals, such as gold, as a possible hedge against further debasement of fiat money.

1By Precariat, we refer to a global “precarious class” of people who are out of work, continually searching for work, or underemployed. Unlike the Karl Marx’s proletariat, based solely on their accumulation of material “stuff” or access to basic services, they are not poor in a global (or even historical) sense. Yet as has been true of most class-based revolts, relative privation and perceived marginalization within one’s community trumps absolute condition. “ Davos man”, a term coined by sociologist Samuel Huntington, symbolizes the global elite which congregates at the World Economic Forum to shape world policy. At this exclusive forum in the Swiss Alps, they look down at the world from above: both because of the high-altitude, but also because of the high incomes and high status that characterize this jet-setting crowd.

Important Disclosures:

This report is neither an offer to sell nor a solicitation to invest in any product offered by FIS Group, Inc. and should not be considered as investment advice. This report was prepared for clients and prospective clients of FIS Group and is intended to be used solely by such clients and prospects for educational and illustrative purposes. The information contained herein is proprietary to FIS Group and may not be duplicated or used for any purpose other than the educational purpose for which it has been provided. Any unauthorized use, duplication or disclosure of this report is strictly prohibited.

This report is based on information believed to be correct, but is subject to revision. Although the information provided herein has been obtained from sources which FIS Group believes to be reliable, FIS Group does not guarantee its accuracy, and such information may be incomplete or condensed. Additional information is available from FIS Group upon request.

All performance and other projections are historical and do not guarantee future performance. No assurance can be given that any particular investment objective or strategy will be achieved at a given time and actual investment results may vary over any given time.